Stunning Info About Other Expenses In Income Statement

:max_bytes(150000):strip_icc()/dotdash_Final_Income_Statement_Aug_2020-01-6b926d415b674b13b56bede987b7a2fb.jpg)

Statement Definition Uses & Examples

/IncomeStatementFinalJPEG-5c8ff20446e0fb000146adb1.jpg)

Year To Date Statement Template Database

Small Business Statement Template New Sample In E For

:max_bytes(150000):strip_icc()/dotdash_Final_Operating_Income_Aug_2020-01-e3ccd90db6224fc8b0bea6dac86e478f.jpg)

Operating Definition

Key Activities Definition Axial Age 800200 Bce Kesaniesan.github.io

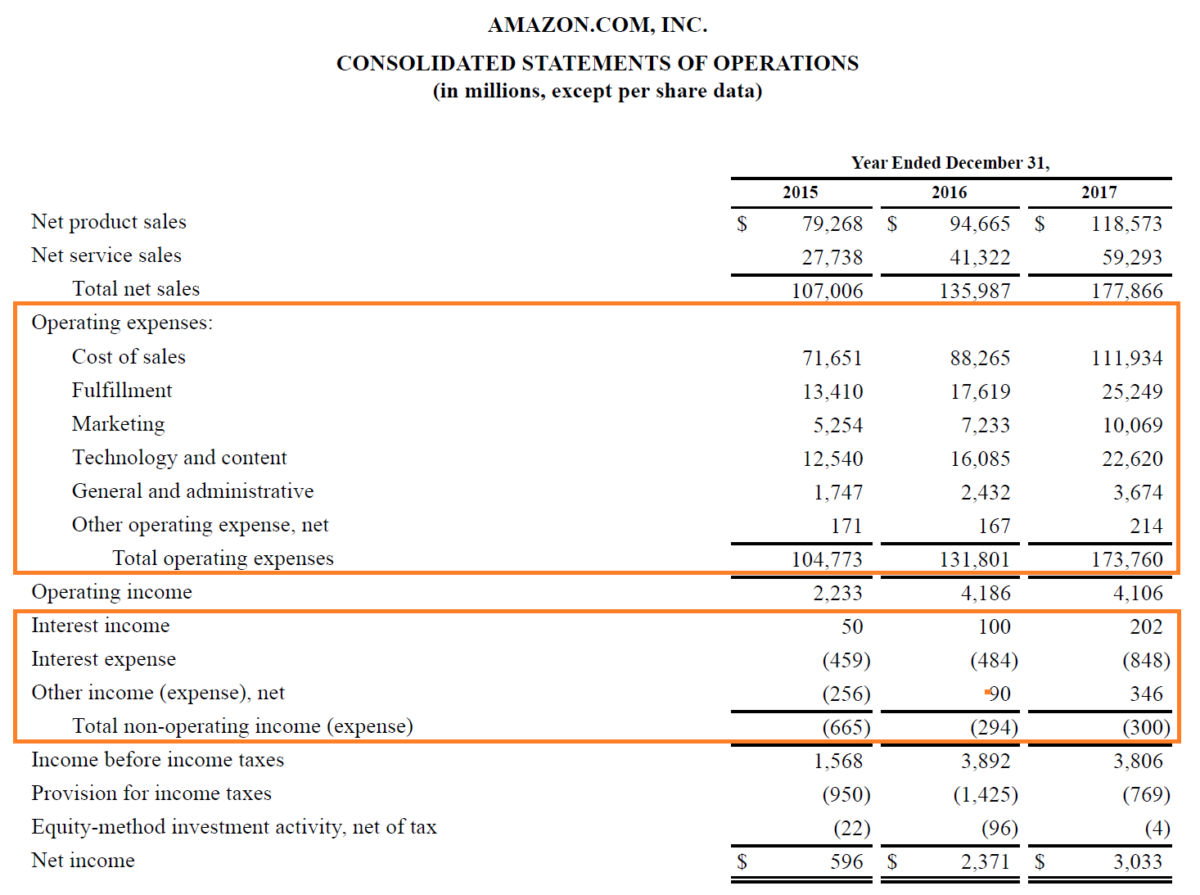

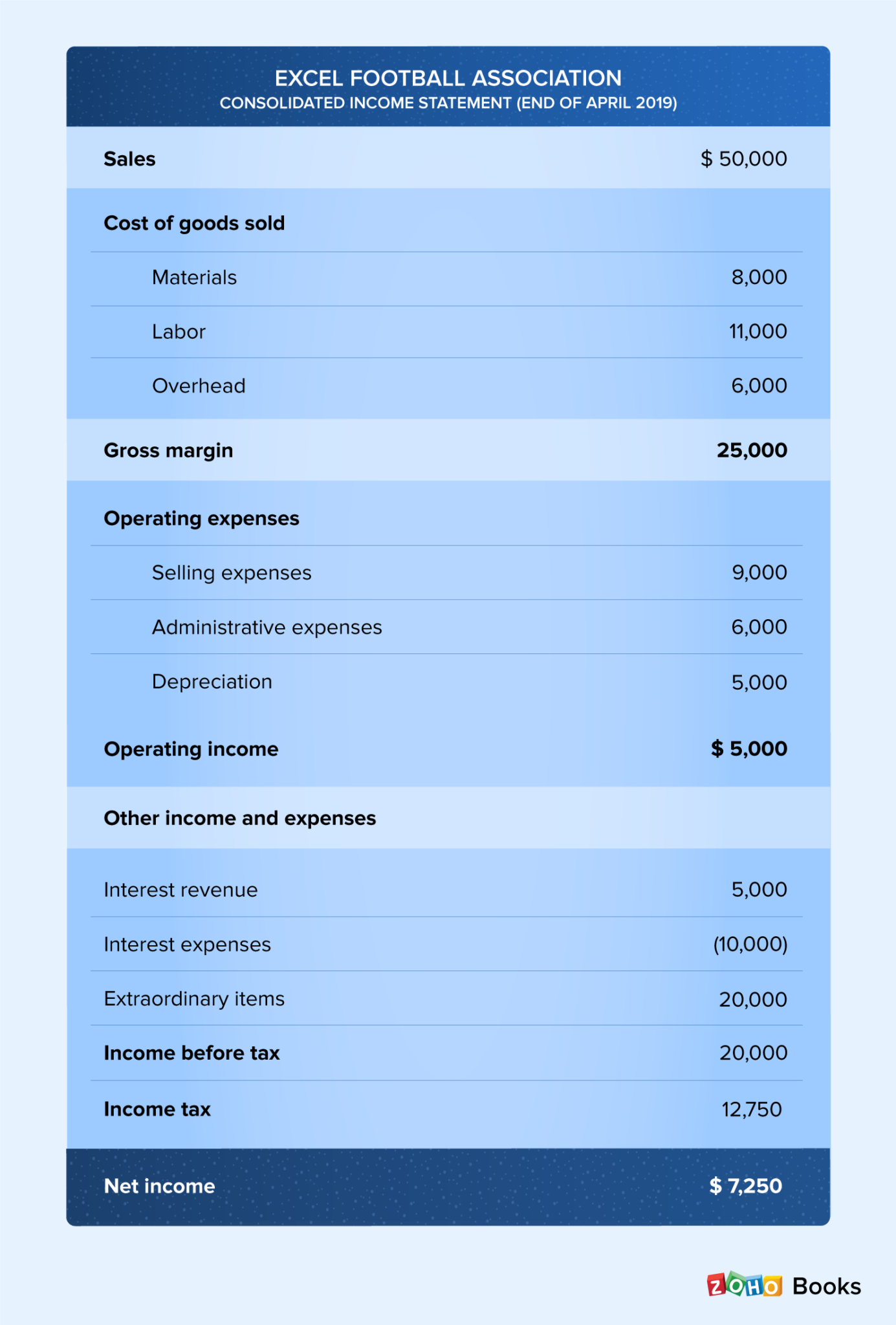

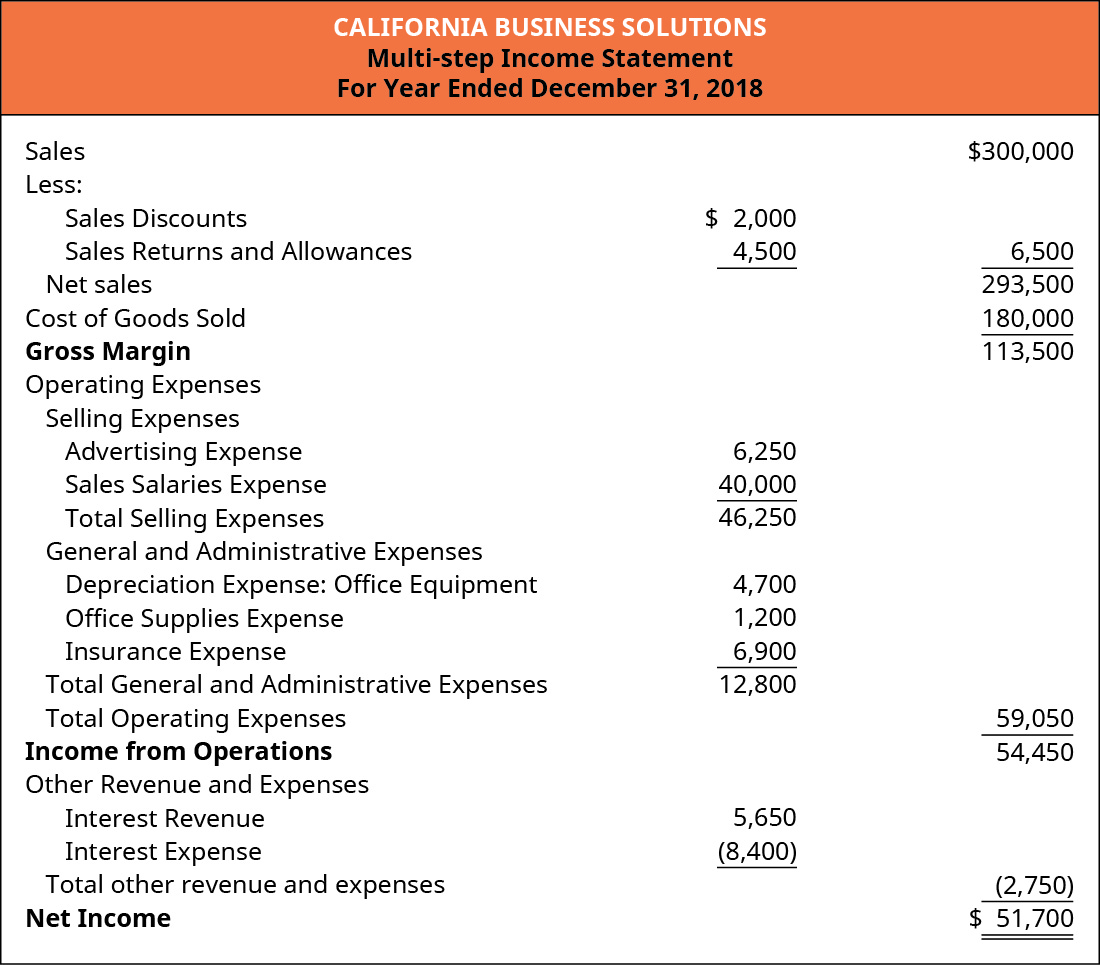

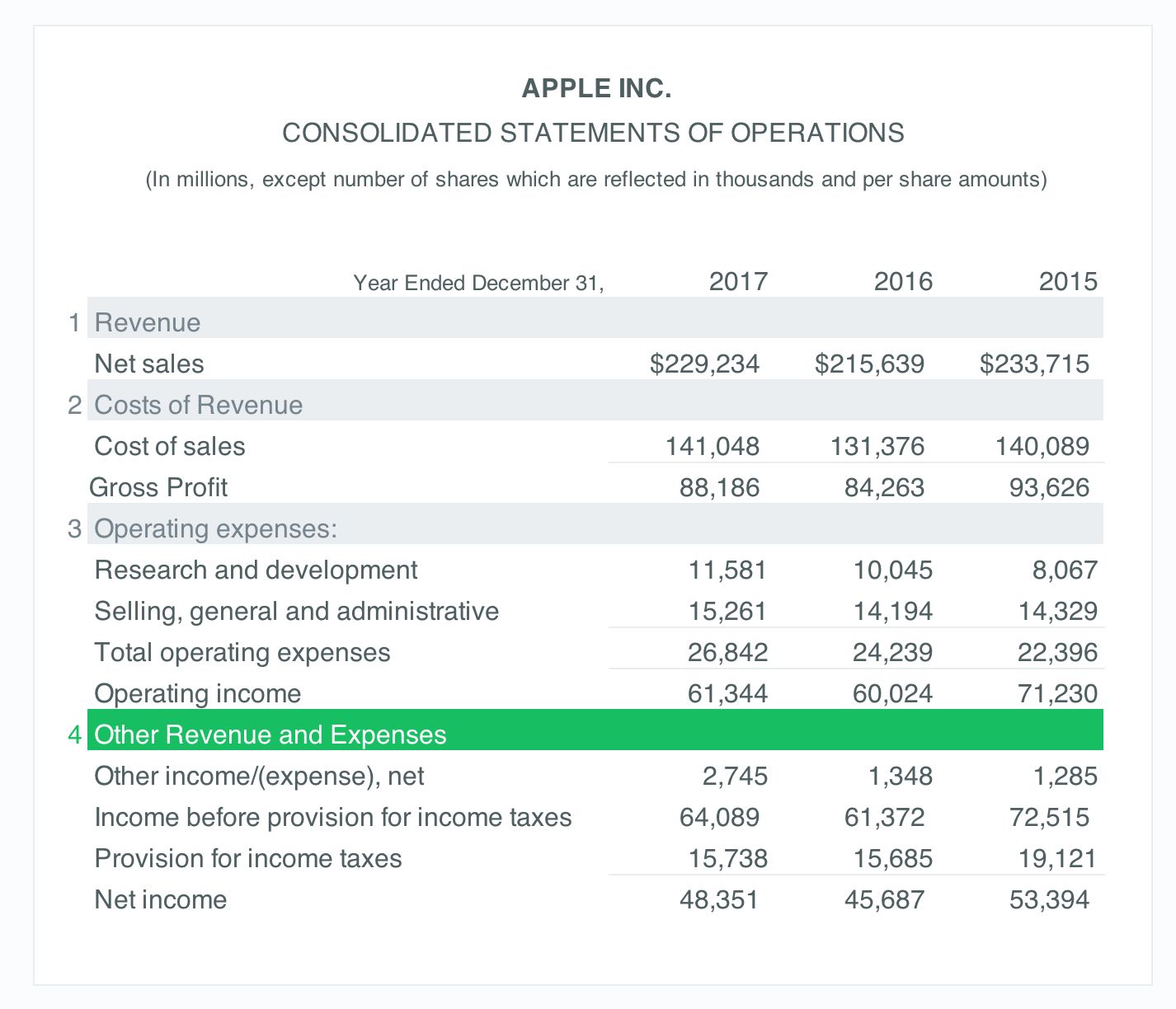

In the income statement, other income is presented after the other gross profit.

Other expenses in income statement. An income statement is another name for a profit and loss statement (p&l). As seen before with best buy, macy's gross profit of $2.14 billion dramatically differs from its net income of $43 million, due to sg&a costs, interest expenses, impairment and restructuring costs. Many key fundamental ratios use information from the income statement.

Medical expenses are deductible only to the extent the total exceeds 7.5% of your adjusted gross income (agi). Sales on credit) or cash. Cogd = (300,000) gross profit = 200,000.

Other income refers to those sources of income of an individual or business which arise out of activities besides the main activity to be recorded separately in schedule 1 of form 1040 or on the income statement. Add up the income tax for the reporting period and the interest incurred for debt during that time. You can look at an income.

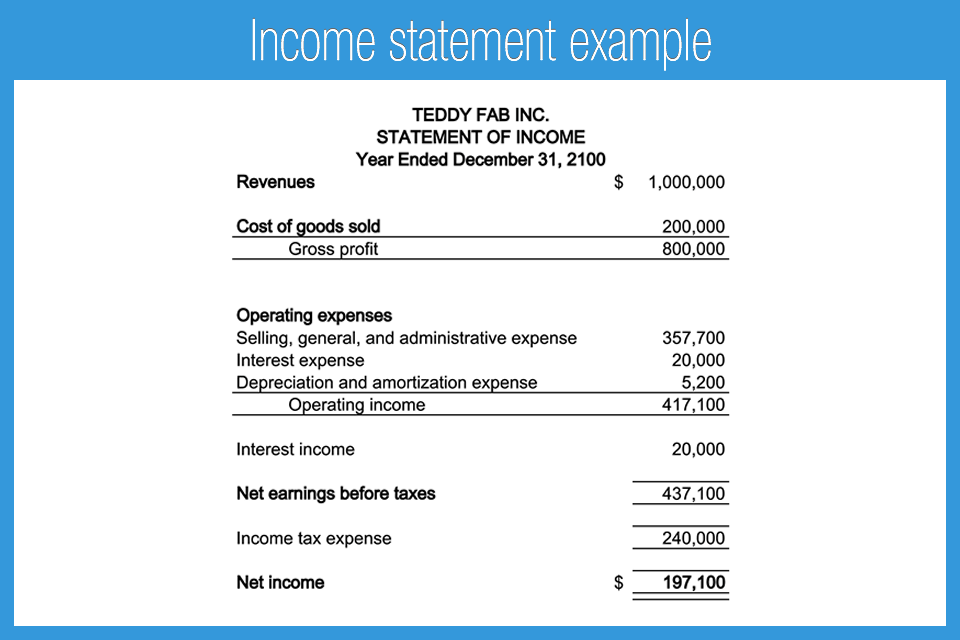

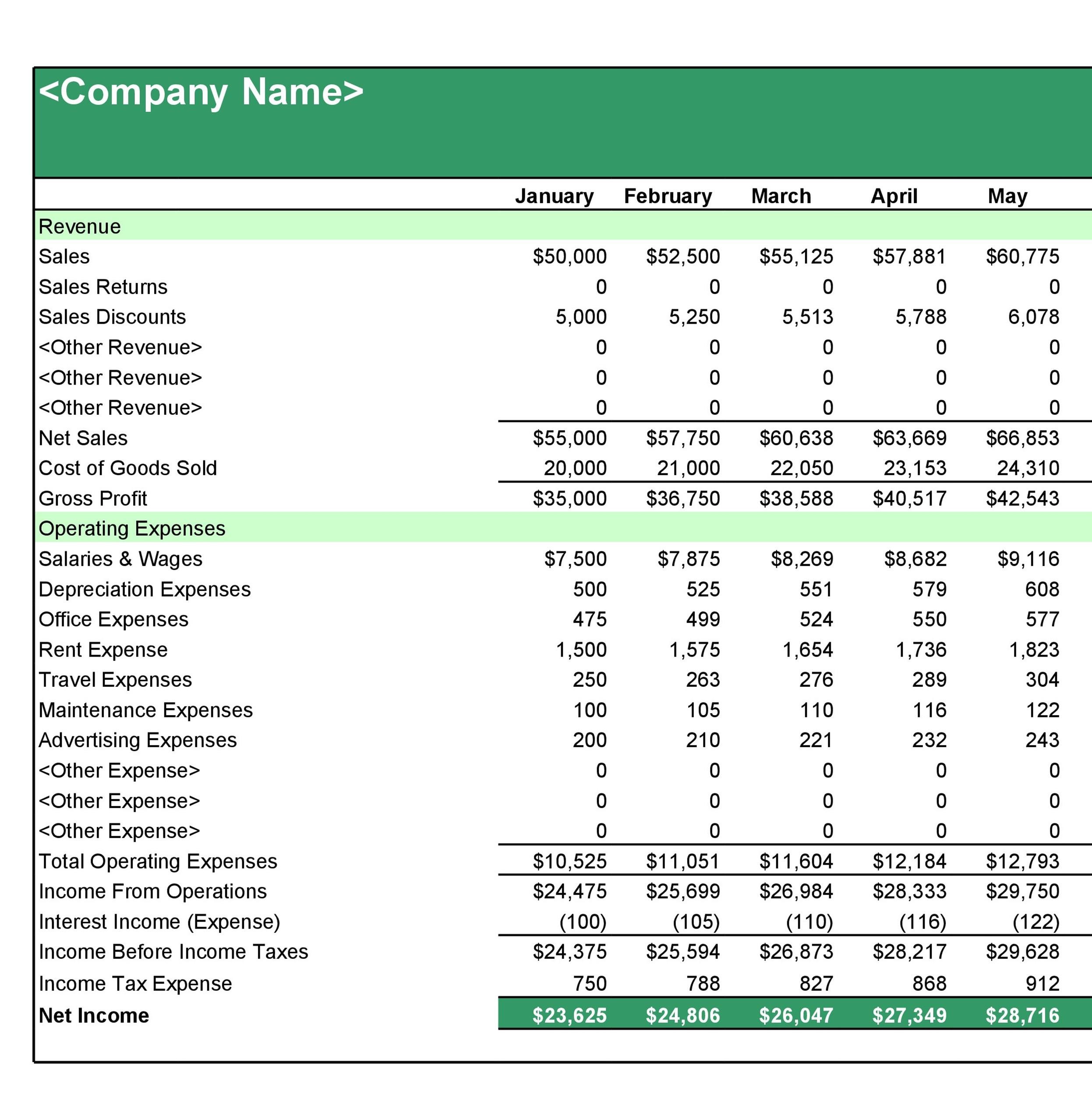

To simplify your understanding of an income statement even further, here is the basic formula that builds an income statement: Revenue minus expenses equals profit or loss. Companies may also present other operating expenses in the income statement.

Your income statement (sometimes called a statement of revenue and expense) shows the revenue your practice earned and the costs associated with running your business. Profit is whatever is left from income once expenses are deduced. Revenue, expenses, gains, and losses.

The income statement communicates how much revenue the company generated during a period and what costs it incurred in connection with generating that revenue. The basic equation underlying the income statement, ignoring gains and losses, is revenue minus expenses equals net income. These expenditures may involve hiring workers, buying supplies and promoting the business.

The financial performance of an entity is measured by profit or loss. How much money a business spent during a reporting period. Revenue minus costs of goods sold.

Accountants record expenses through one of two accounting methods: Some show it at the top of the income statement, just below revenue, whereas others show it below operational expenses. Loss from disposal of an asset or equipment.

You may notice that our expenses exceeded our income in 2023. If revenue is lower than expenses, the company is unprofitable. It conveys to the authorities that the earnings are from activities besides regular taxable income.

Income statements are often shared as quarterly and annual reports, showing financial trends and comparisons over time. The income statement is one of the five financial statements that report and present an entity’s financial transactions or performance, including revenues, expenses, net profit, or loss, and other p&l items for a specific period of time. The income statement is a useful way to see how a company makes money and how it spends it.

And Expenditure Statement Template Free Download Pdf

14 Best Images Of Household Budget Worksheet Excel Monthly Bill

Non Profit Monthly Financial Report Template Personal

Introduction To Financial Statements Accounting Play

Tax Is That Calculated Based On From Continuing

:max_bytes(150000):strip_icc()/TermDefinitions_Incomestatementcopy-9fe294644e634d1d8c6c703dc7642018.png)

Statement How To Read And Use It (2023)

Sample Disclosure Statement With Expenses By Nature (18

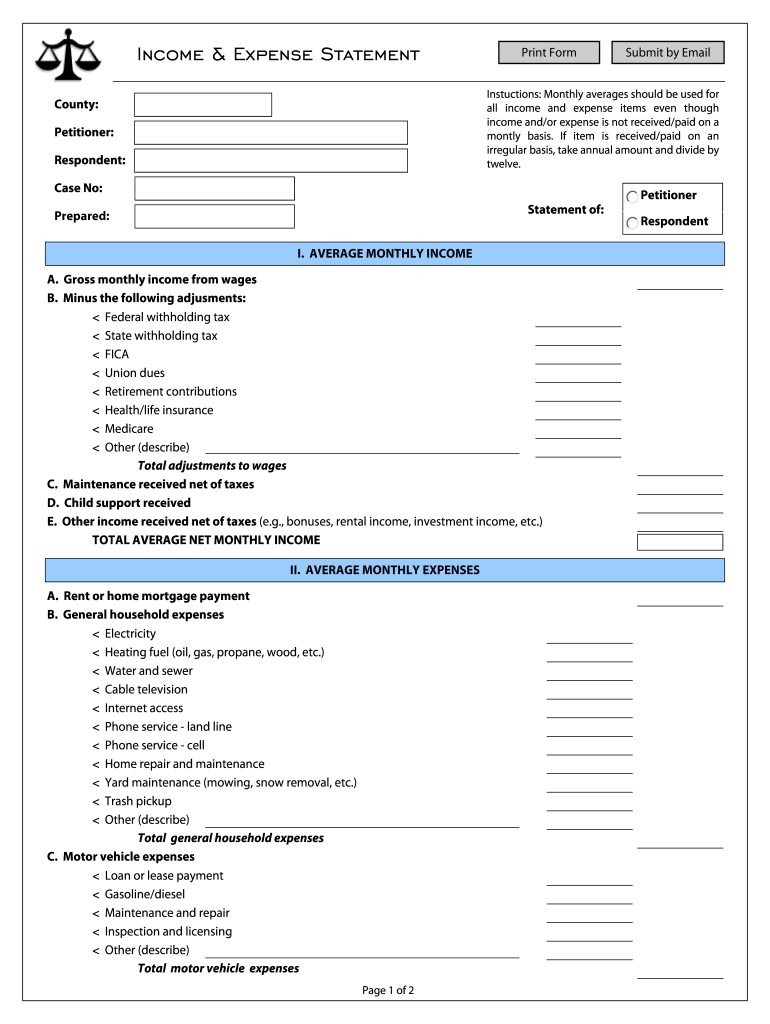

Free And Expense Forms Statement Template

Lo 6.6 Describe And Prepare Multistep Simple Statements For

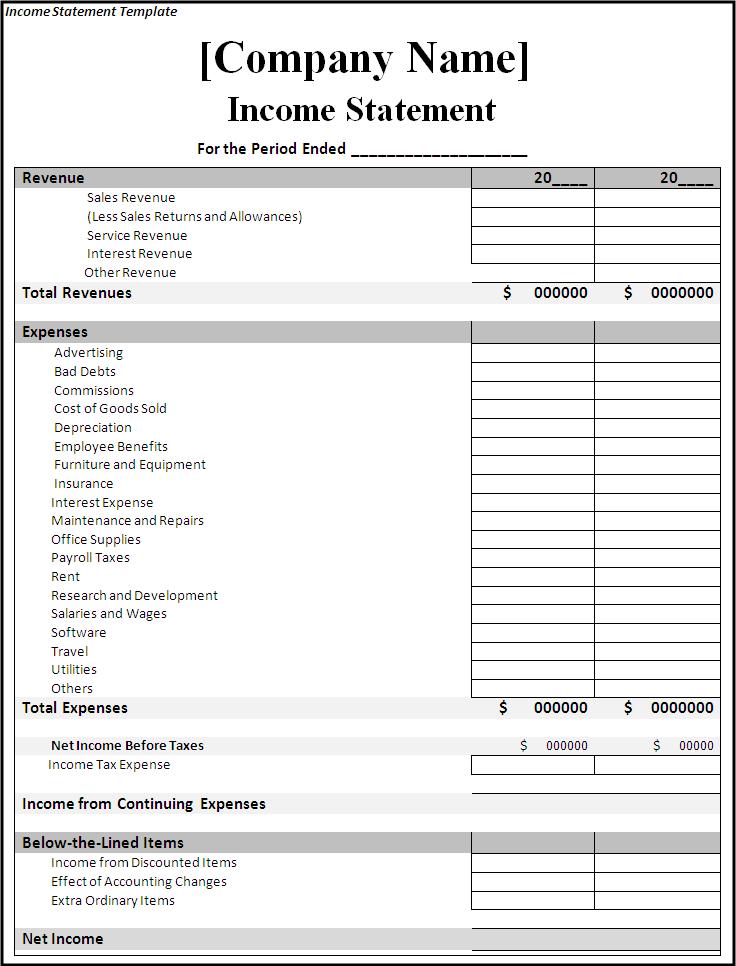

41 Free Statement Templates & Examples Templatelab

Expense Statement 20052024 Form Fill Out And Sign Printable

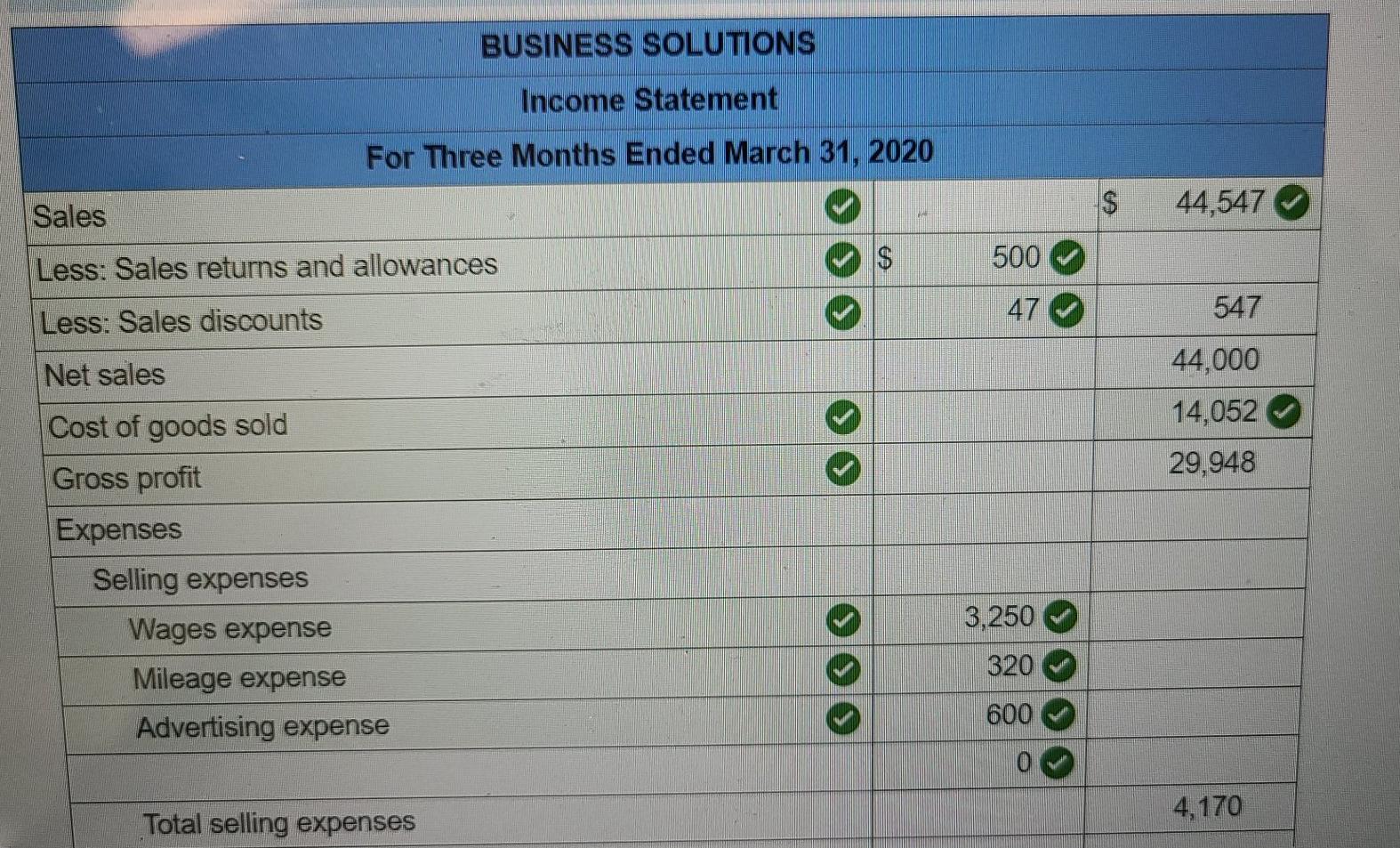

Solved 4. Prepare An Statement (from The Adjusted