Amazing Tips About Adjustment In Financial Statements

Relationship Between Financial Statements Double Entry Bookkeeping

Quadserv Financial Statement Analysis That Small Businesses Should Know.

Ideal In Preparing Financial Statements From The Trial Balance, Balance

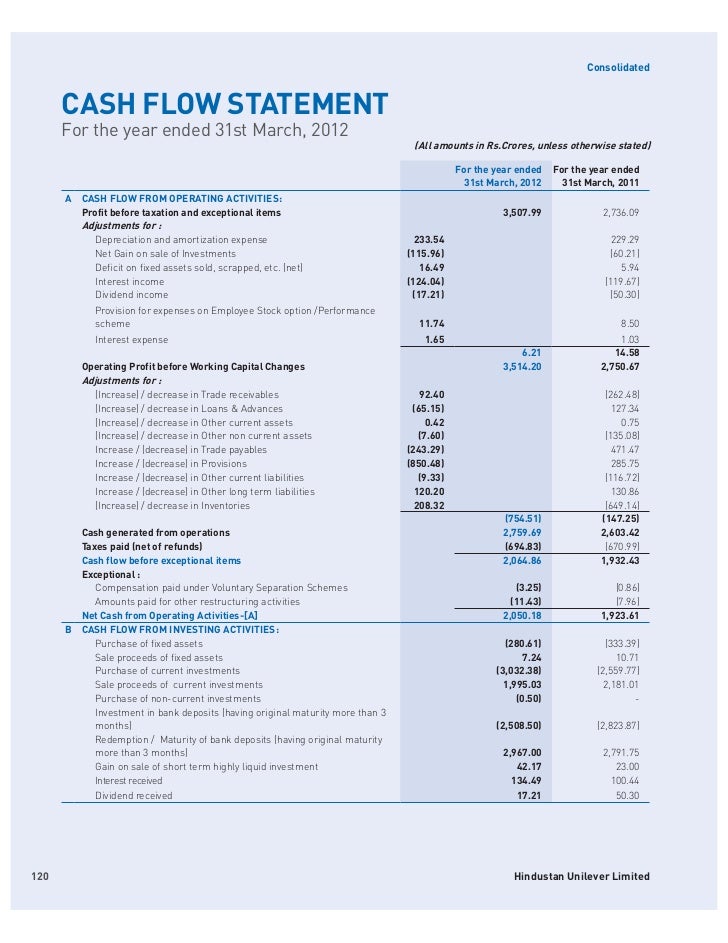

Ifrs Interest Paid Cash Flow Statement, Barclays Stockbrokers Foreign

Lukeko Chapter 4 Adjustments, Financial Statements, And The Quality

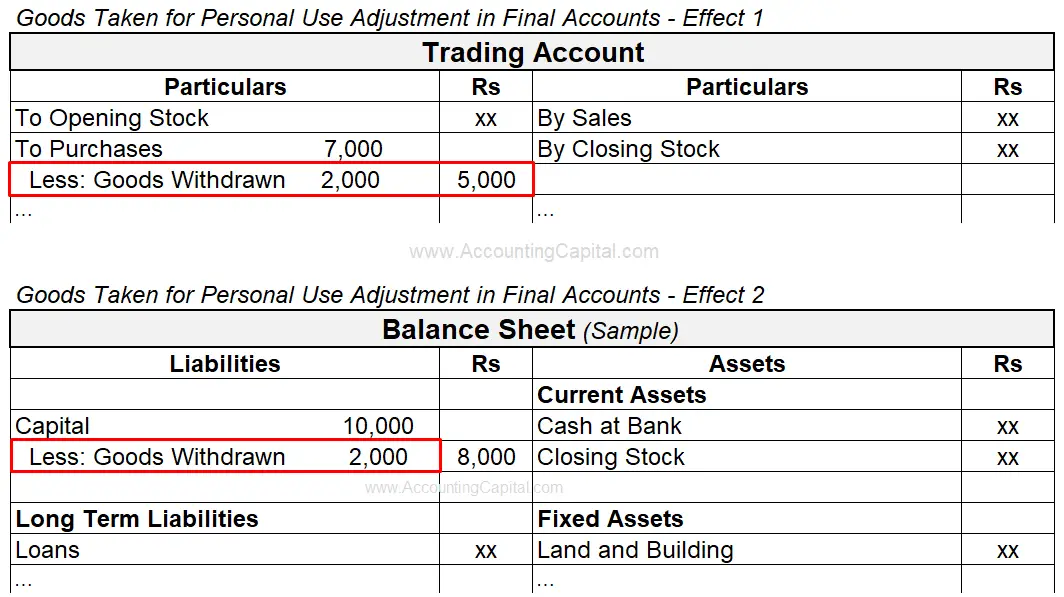

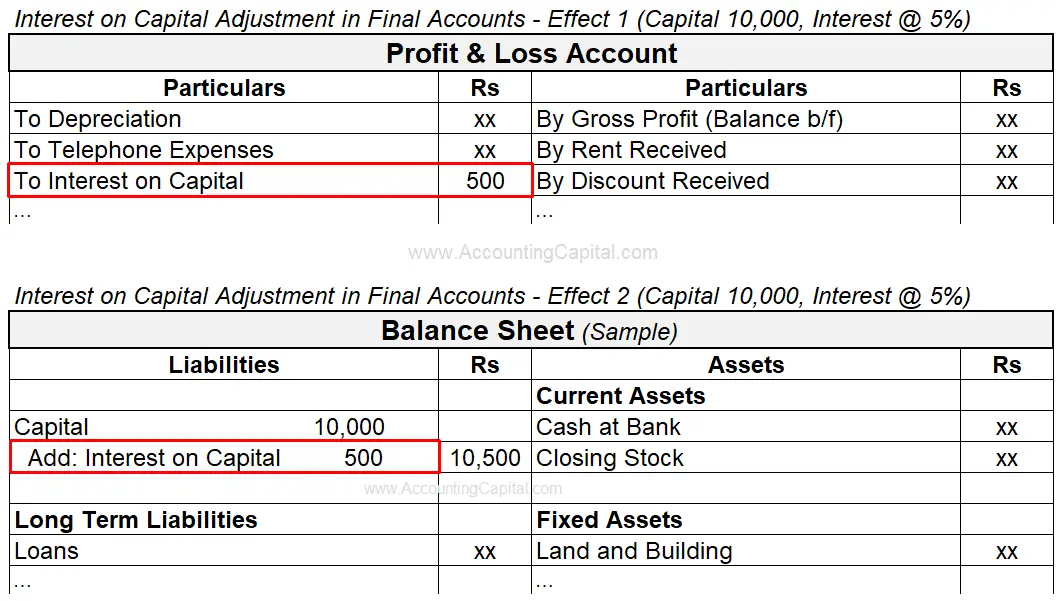

Adjustments In Final Accounts (examples, Explanation, More..)

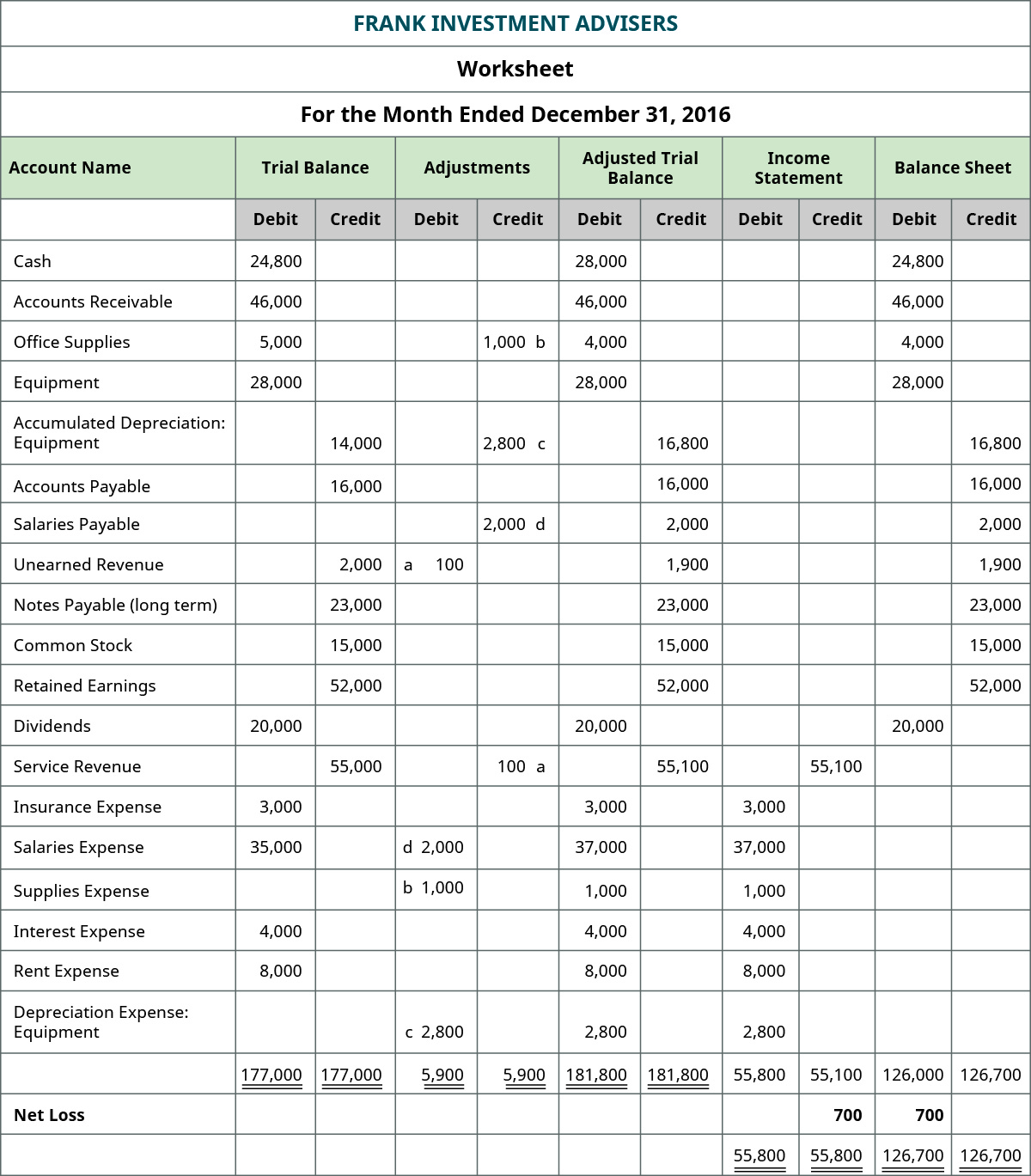

The adjustments total of $2,415 balances in the debit and credit columns.

Adjustment in financial statements. One important accounting principle to remember is that just. To get the numbers in these. Adjustments to financial statements inventory.

Types of adjusting journal entries 1. Analysts frequently make adjustments to a company’s reported financial statements when comparing those statements to those of another company that uses. Record and post the common types of adjusting entries;

In this publication, we provide an. Adjusting entries update accounting records at the end of a period for any transactions that have not yet been recorded. Adjustments in financial statement:

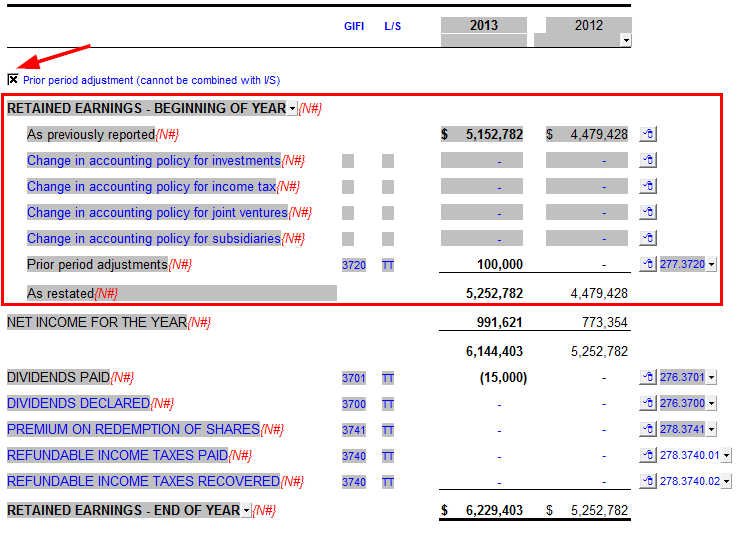

An adjustment to two figures are now needed. A prior period adjustment is used to adjust financial statements from a previous accounting period to reflect changes or corrections that were not recorded in. To know the correct net profit or net loss of the business for an accounting year.

Accounting adjustments are required because of the following purposes: Adjustments for accounting changes and error correction for financial statements to be useful, they must apply accounting policies consistently and must be comparable. The main objective of preparing a financial statement is to know about the financial position of a company and find out the.

Accounting changes and errors in previously filed financial statements can affect the comparability of financial statements. Discuss the adjustment process and illustrate common types of adjusting entries; The process to ensure that all accounts are reported accurately at the end of the period is called the adjusting process.

Adjustments in final accounts refer to changes made to certain financial entries at the end of an accounting period. These adjustments are crucial for presenting a true and fair view. Every adjusting entry will have at least one income statement account and one balance sheet account.

Bad debts appear as an adjustment outside the trial balance. The cost of sales consists of opening inventory plus purchases, minus. Get nature and significance of.

This is a very common adjustment. The statement of profit or loss must include the expenses relating to the period, whether. At the end of an.

The next step is to record information in the adjusted trial balance columns. The amount goes into the statement of profit or loss as an expense (it. Financial statement with adjustment with.

Series 1 Fasb Nonprofit Financial Statement Project Presentation Of

Adjustments Financial Statements Accounting Education

Please Find The Solution Also Explain How 4th Adjustment's

How Do I Record A Prior Period Adjustment In My Jazzit Financial

Adjustment Financial Statements In Powerpoint And Google Slides Cpb

Give Me Answer Of Adjustment 4 921 Am Adjustments In Preparation

Nice Prior Year Adjustment Disclosure Accounting For Convertible Loan

Adjustments In Final Accounts (examples, Explanation, More..)

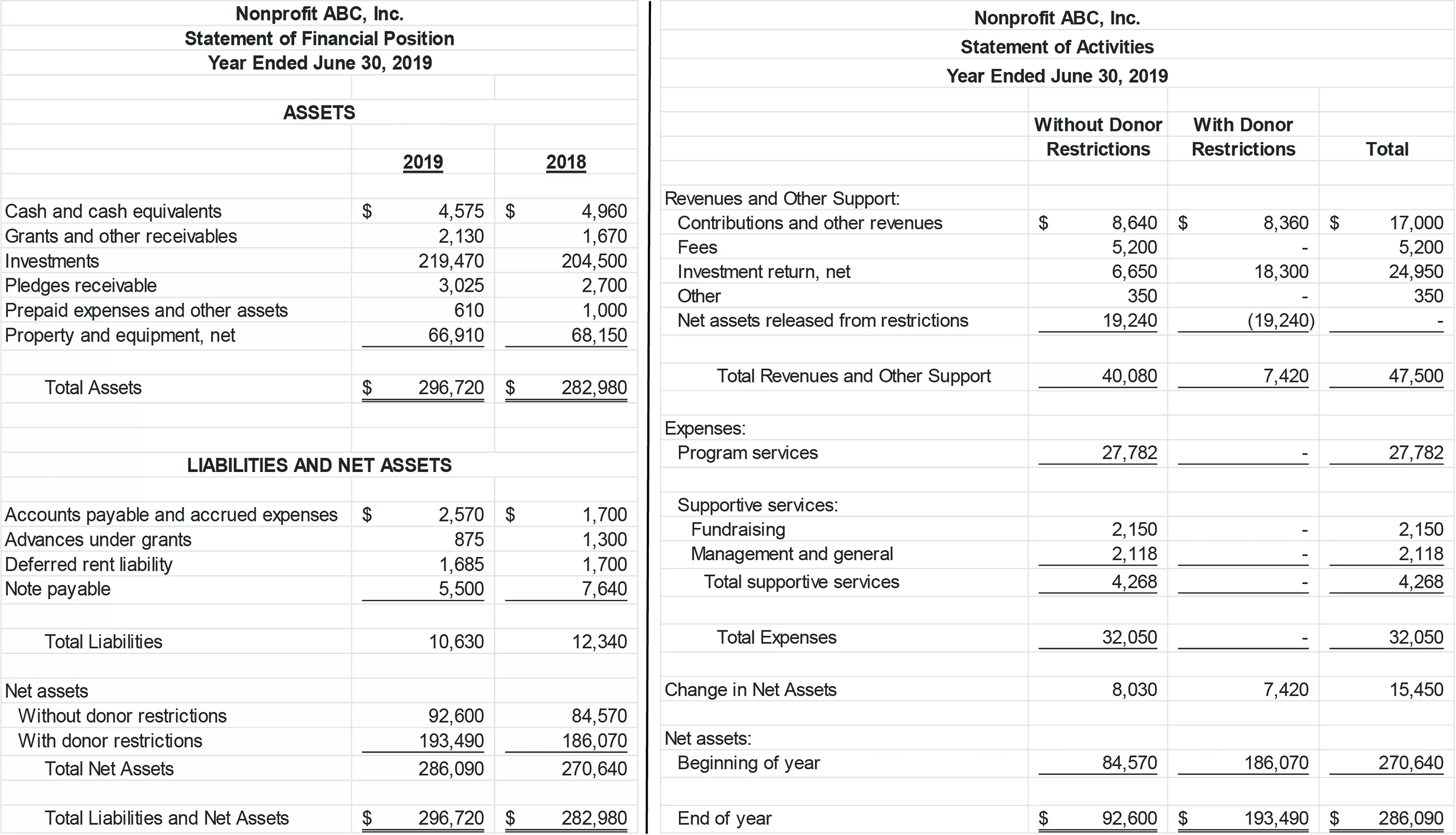

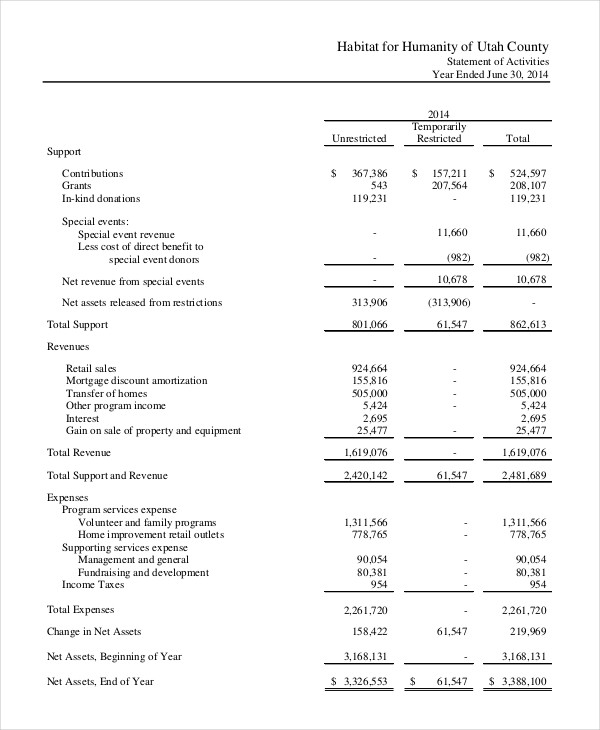

How To Create Nonprofit Financial Statements (5 Best Examples) Examples

14.1 Financial Statement Analysis Business Libretexts

14.1 Financial Statement Analysis Business Libretexts

Arc 70 The Definitive Guide To Preparations Cpa Hall Talk

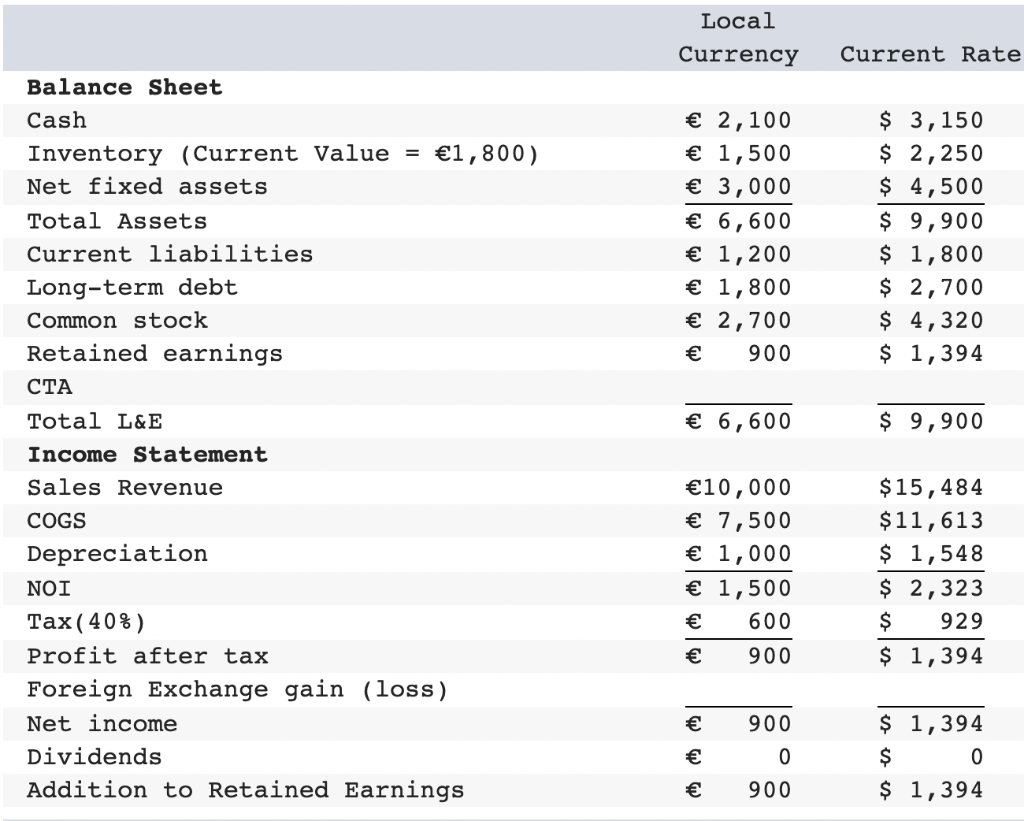

Solved Calculate The Cumulative Translation Adjustment For