Fabulous Tips About Ias Ifrs 16

Ias 17 And Ifrs 16 Comparison Youtube

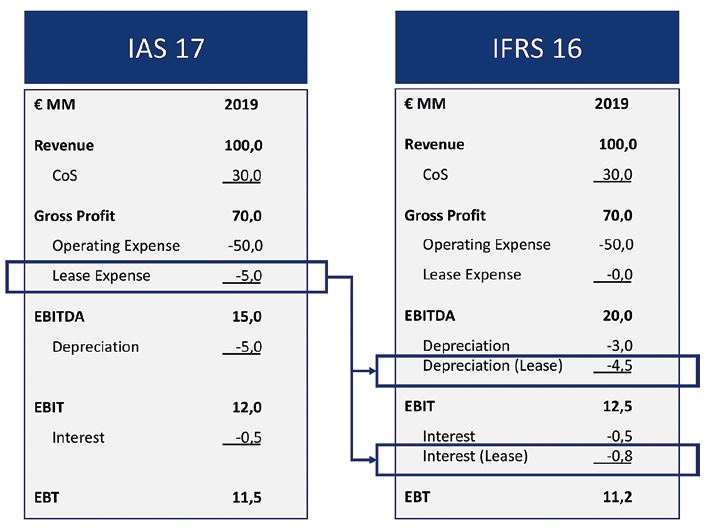

The Key Differences Between Ifrs 16 And Ias 17 Opal Wave

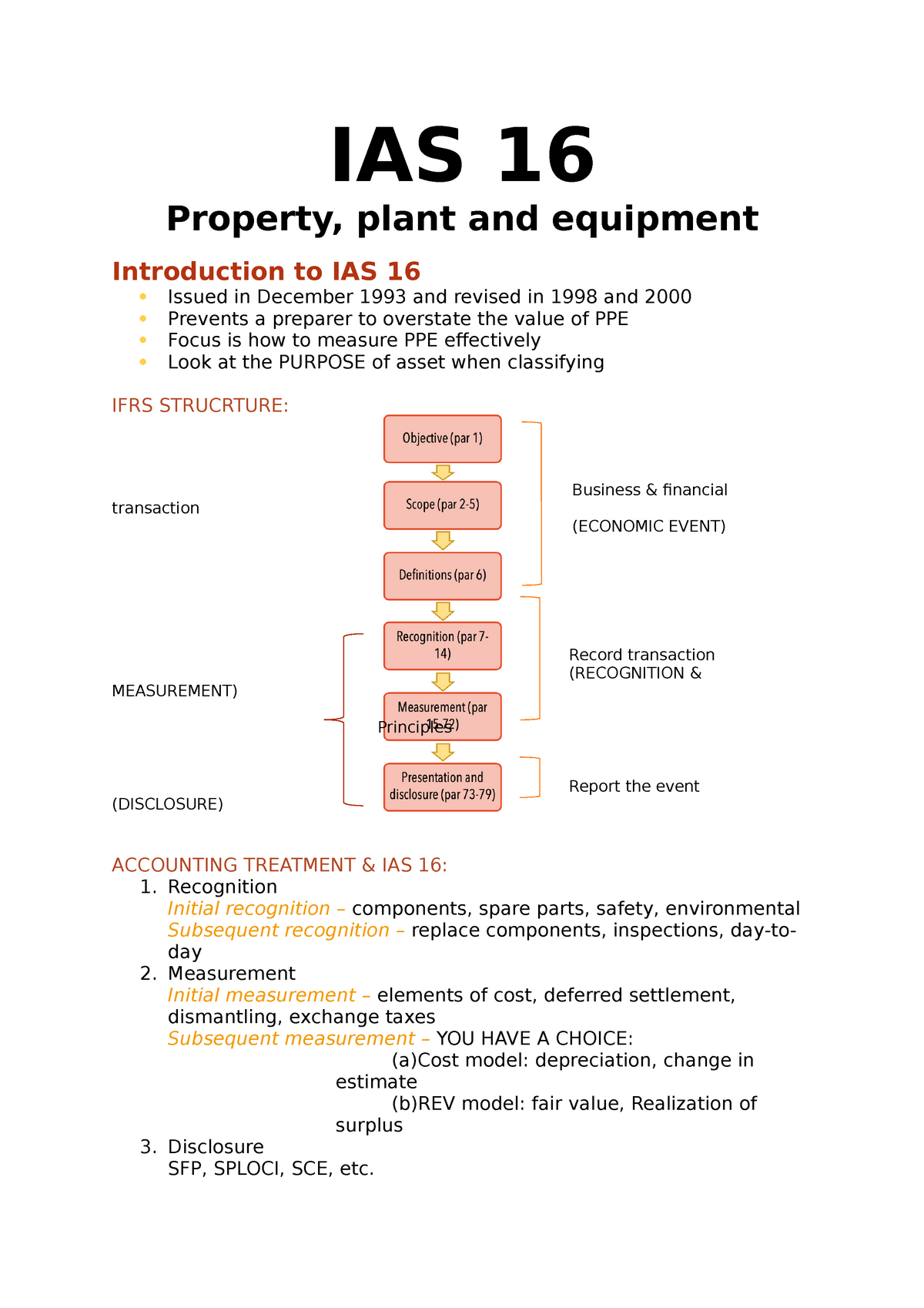

Ias 16 Word Summaries From Slides Property, Plant And

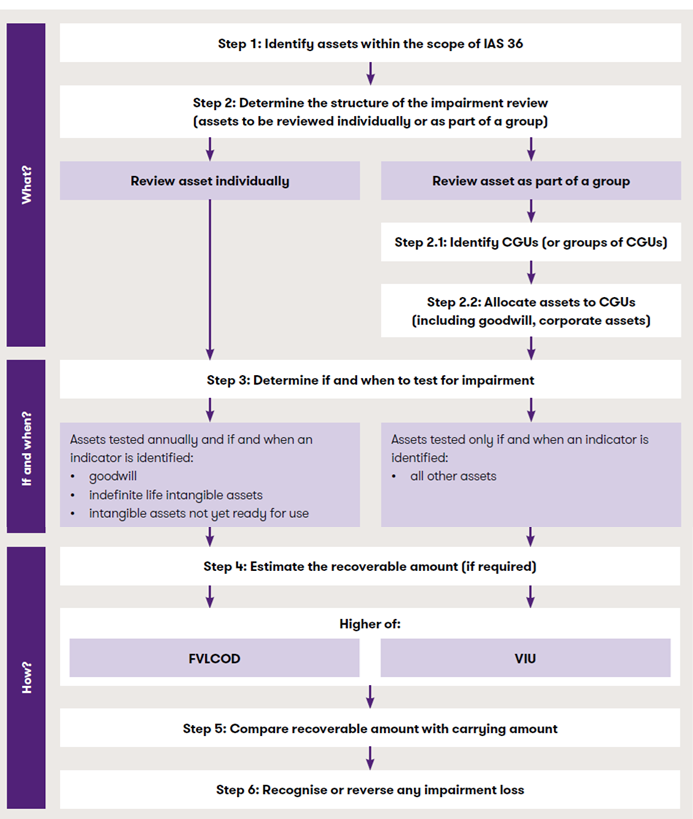

Ias 36 Overview Of The Standard Grant Thornton Singapore

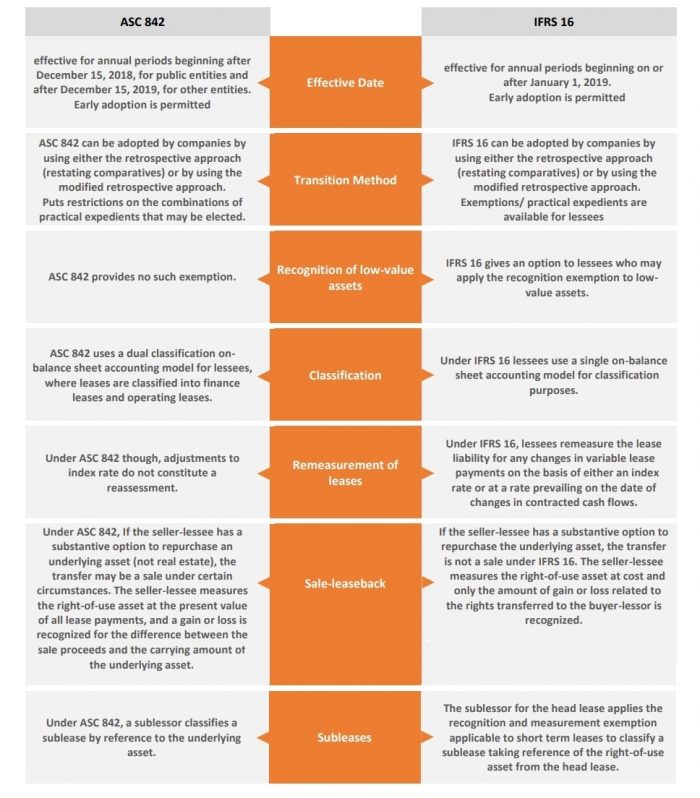

Comparative Analysis Asc 842, Ifrs 16 & Ias 17 Revgurus

Summaries Of Ias And Ifrs Acca Study Material

Contain, leases that should be accounted for in accordance with ias 17.

Ias ifrs 16. In january 2016 the board issued ifrs 16 leases. Service concession arrangements (see ifric 12 service. The cost of property, plant and equipment (also known as ‘pp&e’) is composed of the following elements according to ias 16.16:

At the commencement of a lease, a lessee recognises the following: When applying ifrs 16 using the modified retrospective approach, entities must reconcile the operating lease commitments reported under ias 17 with the lease. Proceeds before intended use (amendments to ias 16) which prohibit a company from deducting from the cost of.

Ifrs 16 provides a comprehensive guide for identifying lease arrangements and how it should be used in financial statements for both the lessees and lessors. Leases of biological assets held by a lessee (see ias 41 agriculture); For entities using the revaluation model, the disclosure.

International accounting standard 16property, plant and equipment charge for a period is usually recognised in profit or loss. However, sometimes, the future economic benefits. Ias 16 2021 issued ifrs standards (part a) ias 16 property, plant and equipment in april 2001 the international accounting standards board (board) adopted ias 16 property,.

The objective of ias 16 is to prescribe the accounting treatment for property, plant, and equipment. In may 2020, the board issued property, plant and equipment: Ias 16.79 also encourages (but does not mandate) the provision of additional information.

Revenue superseded in 2018 by ifrs 15: Leases superseded in 2019 by ifrs 16: Definition of a lease—substitution rights (ifrs 16) economic benefits from use of a windfarm (ifrs 16) ibor reform and its effects on financial reporting—phase 2;.

The international accounting standards board (iasb) has issued 'lease liability in a sale and leaseback (amendments to ifrs 16)' with amendments that clarify how a seller. The principal issues are the recognition of assets, the determination of their. Ifrs 16 replaces ias 17, ifric 4, sic‑15 and sic‑27.

Ifrs 16 sets out the principles for the recognition, measurement, presentation and disclosure of leases. Bearer plants (amendments to ias 16 and ias 41) clarification of acceptable methods of depreciation and amortisation (amendments to ias 16 and ias 38). Sales proceeds from testing an asset (ias 16) lease term and useful life of leasehold improvements (ifrs 16 and ias 16)

Ifrs 16 Leases Youtube

List Of Ifrs And Ias International Financial Reporting Standards

Analytix & Ifrs9 Analytix.gr

Ias / Ifrs For Greenhorns 2. Edition Revised And Expanded With 9

![[PDF] Comparison of IAS 39 and IFRS 9 The Analysis of Replacement](https://d3i71xaburhd42.cloudfront.net/67b3ca92d6a9916b419602abe09bd860d20fc48b/3-Table1-1.png)

[pdf] Comparison Of Ias 39 And Ifrs 9 The Analysis Replacement

La Nouvelle Norme Ifrs 15

Ifrs 16 Practical Example And Changes Comparison With Ias 17 Youtube

Ias 17 Vs Ifrs 16 Lease Differences Pdf

Impact Of New Lease Accounting Under Ifrs 16

Insight All Courses

How Digitisation Helps You Tackle Ifrs 9 Challenges

Lease Accounting Under Ifrs 16 A Leap Towards Transparency! Vinod

Ifrs 16 Consolidation Financial Statement Alayneabrahams