Casual Tips About Rectification Of Errors Before Preparation Trial Balance

Rectification Of Errors Accountancy Knowledge

Solution Trial Balance And Rectification Of Errors Studypool

Solution Trial Balance And Rectification Of Errors Studypool

Rectification Of Errors Accountancy Knowledge

Mcq Questions For Class 11 Accountancy Chapter 6 Trial Balance And

Ncert Solutions For Class 11 Accountancy Chapter 6 Trial Balance And

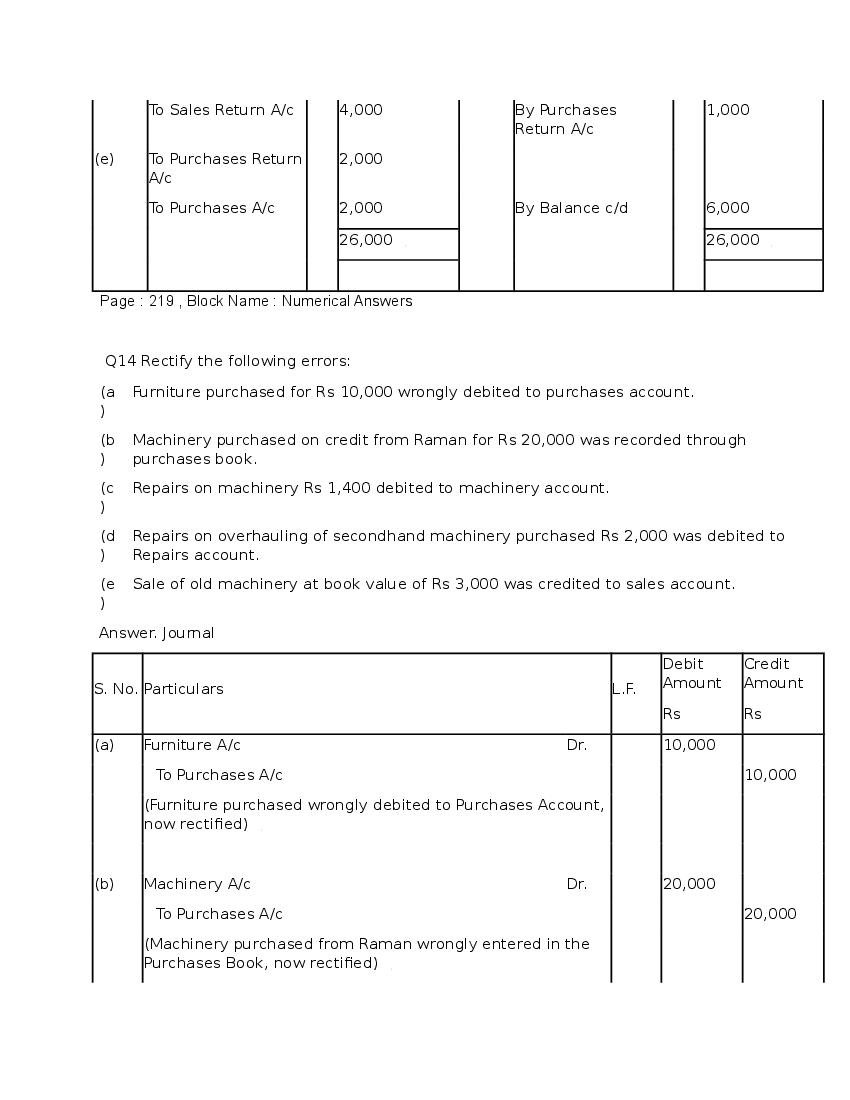

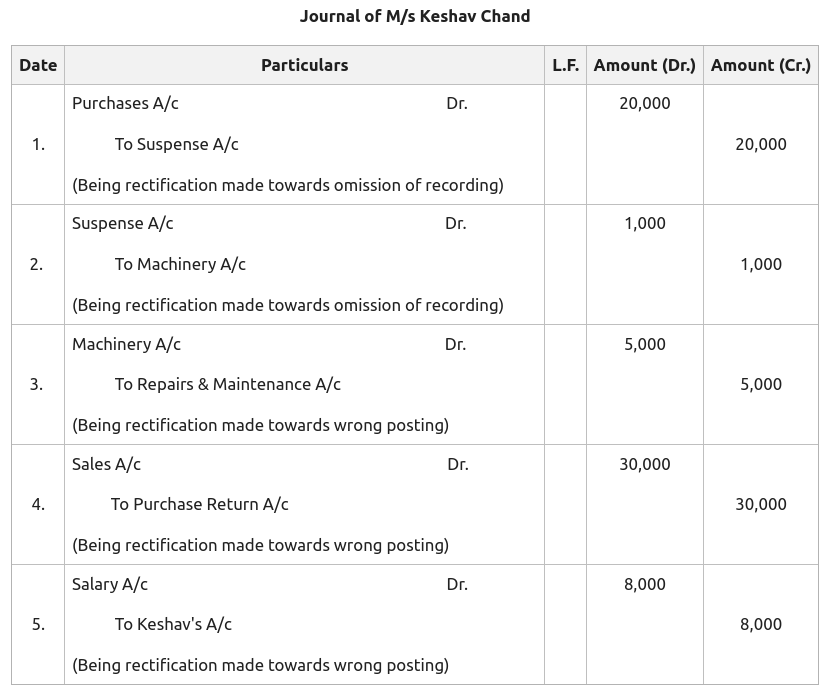

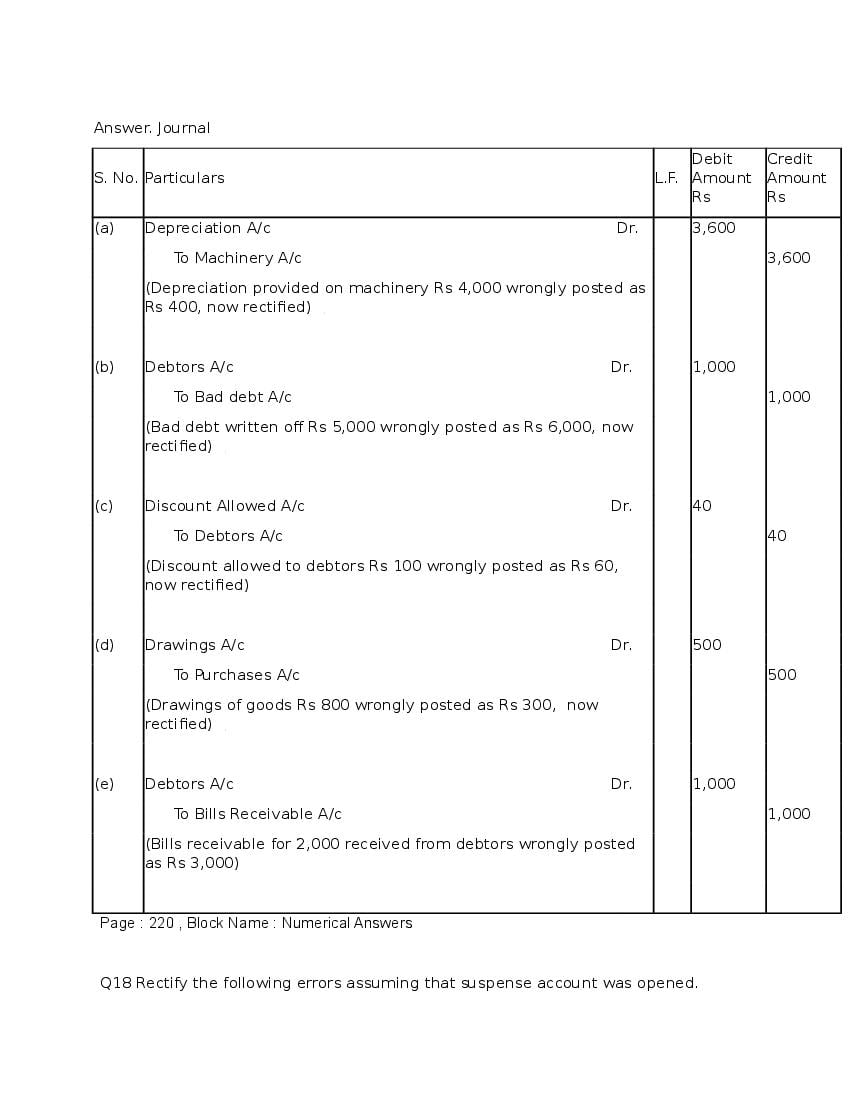

The solution for all the rectification of errors is as follows journal recordings.

Rectification of errors before preparation of trial balance. The error or the errors have. B) after trial balance but before the final account are drawn. It thus verifies that both.

In this stage, errors are located before transferring the difference in the trial balance to. (i) wages paid for construction of office building debited to wages. Rectification of errors problems pdf download.

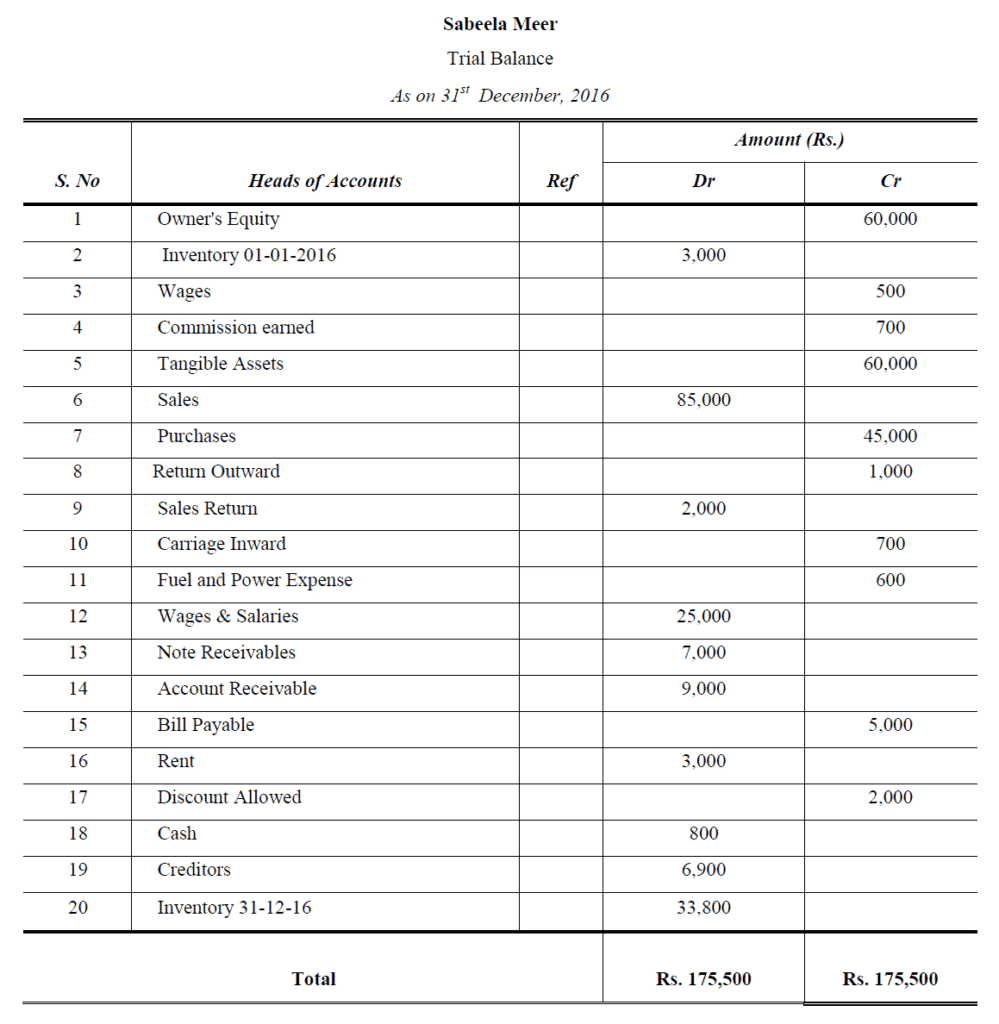

C) after final accounts, i.e., in the next accounting period. Trial balance and rectification of errors trial balance is a statement which accounts all the balances of the personal account, real account, and nominal account regardless of.

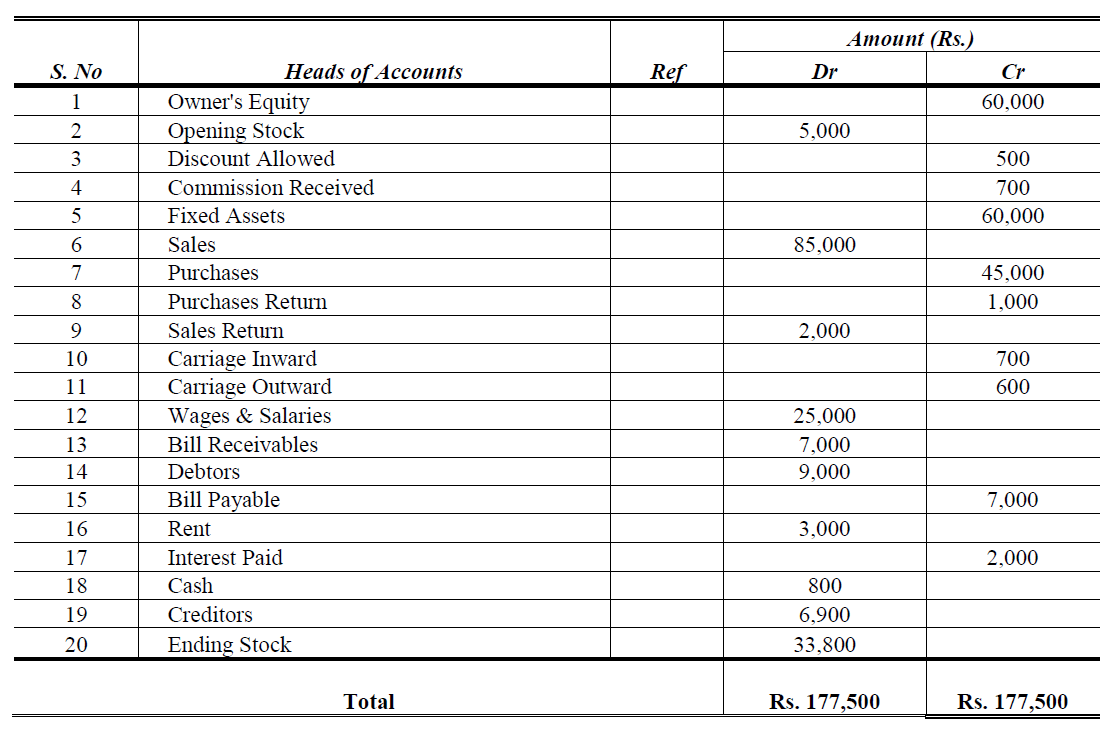

Pass the journal entries to rectify the following errors detected during preparation of the trial balance : Stages of rectification of errors. Trial balance and rectification of errors preparation of trial balance a trial balance is a statement that shows the total debit and total credit balances of accounts.

On the basis of rectification of errors, we can classify the errors into the following two broad categories: The following trial balance has been drafted by a book keeper for the preparation of final accounts of a noman ltd. Trial balance and rectification of errors in case of an untallied trial balance, we know that at least one error has occurred.

When errors are detected before the preparation of the trial balance, it should be ascertained whether. The trial balance is a tool for verifying the correctness of debit and credit amounts. Whenever the trial balance does not tally management should know that there is at least one error in the accounting process.

Rectification before the preparation of trial balance: A) before preparation of trial balance; Trial balance and rectification of errors.

The final step before the preparation of the final accounts of the organization is the preparation of the trial. To help in the rectification of errors:

Rectify the errors and prepare suspense account to ascertain the difference in trial balance. Of preparing trial balance ;

Errors not affecting the trial balance; Rectify the following errors before the preparation of trial balance: Rectification of errors significance of agreement of trial balance and searching of errors the final step before the preparation of the final accounts of the organization is.

Ncert Solutions For Class 11 Financial Accounting Trial Balance And

Detection And Rectification Of Errors In Trial Balance

Experts Pls Answer This Question Accountancy Trial Balance And

Trial Balance And Rectification Of Errors Teaching Resources

(pdf) Sssc.uk.gov.in · Trial Balance And Rectification Of Errors

Ncert Solutions For Class 11 Financial Accounting Trial Balance And

Rectification Of Errors Accountancy Knowledge

Rectification Of Errors After Preparation Trial Balance But Before

Ncert Solutions For Class 11 Financial Accounting Trial Balance And

Trial Balance Mcqs Rectification Of Errors Financial

Chapter 17 Part 2 Rectification Of Errors One Sided Error Before

Ncert Solutions For Class 11 Accountancy Chapter 6 Trial Balance And

Idbi Balance Sheet Financial Statement Alayneabrahams