Peerless Tips About Ias Cash Flow Statement

Ias 7 Statement Of Cash Flows

Ias 7 Statement Of Cash Flows Updated Video Link In The Description

Treatment Of Provision For Doubtful Debts In Cash Flow Statement

![IAS 7 Cash Flows IFRS [ International Accounting Standard 7 ] IFRS 7](https://i.pinimg.com/originals/51/c4/e3/51c4e391a1d330685d14094d830b258d.jpg)

Ias 7 Cash Flows Ifrs [ International Accounting Standard ]

Ias 7 Cash Flow Statement

Ias 1 Presentation Of Financial Statements Acca Study Material

All of the agenda decisions that relate to this accounting standard can be found by expanding the link below.

Ias cash flow statement. Restricted cash refers to cash and cash equivalent balances that have usage constraints. It requires the presentation of changes in cash and cash equivalents in the form of statement of cash flows; Ceo statement “in 2023, we delivered another strong and resilient performance.

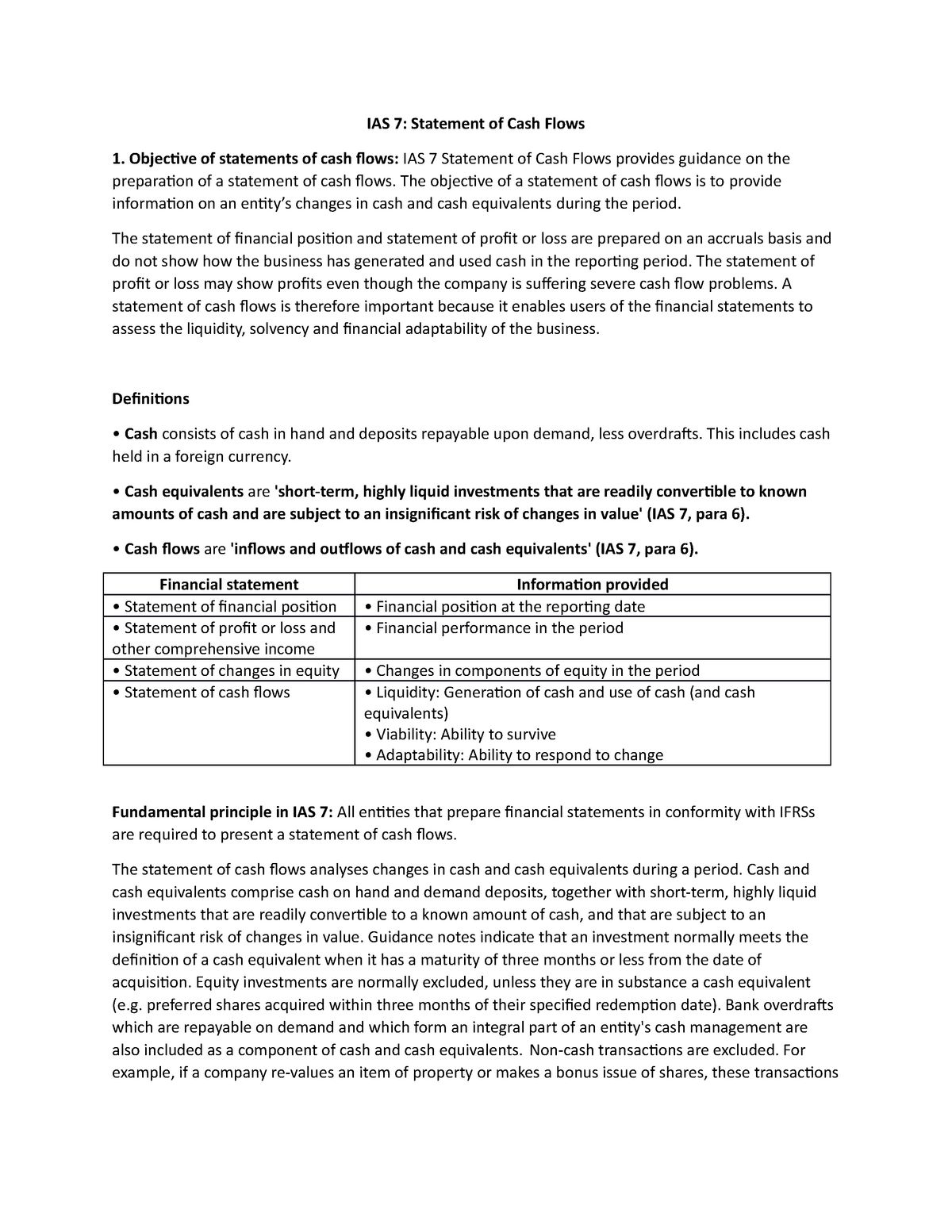

Statement of cash flows (ias 7) cash and cash equivalents. A cash flow statement helps you understand how the entity generates and uses cash and can also indicate the amount, timing and certainty of future cash flows. The statement of cash flows analyses changes in cash and cash equivalents during a period.

This course will walk you through the main concepts and elements of statement of cash flows using practical examples and interim tests to enhance understanding. A statement of cash flows is part of an entity’s complete set of financial statements in accordance with paragraph 10 of ias 1 ‘presentation of financial statements’ (ias 1.10). Income statement and free cash flow.

A statement of cash flows allows users to assess the ability of an entity to: Both of these issues related to classification under ias 7 statement of cash flows and included: Ias 7 statement of cash flows requires an entity to present a statement of cash flows as an integral part of its primary financial statements.

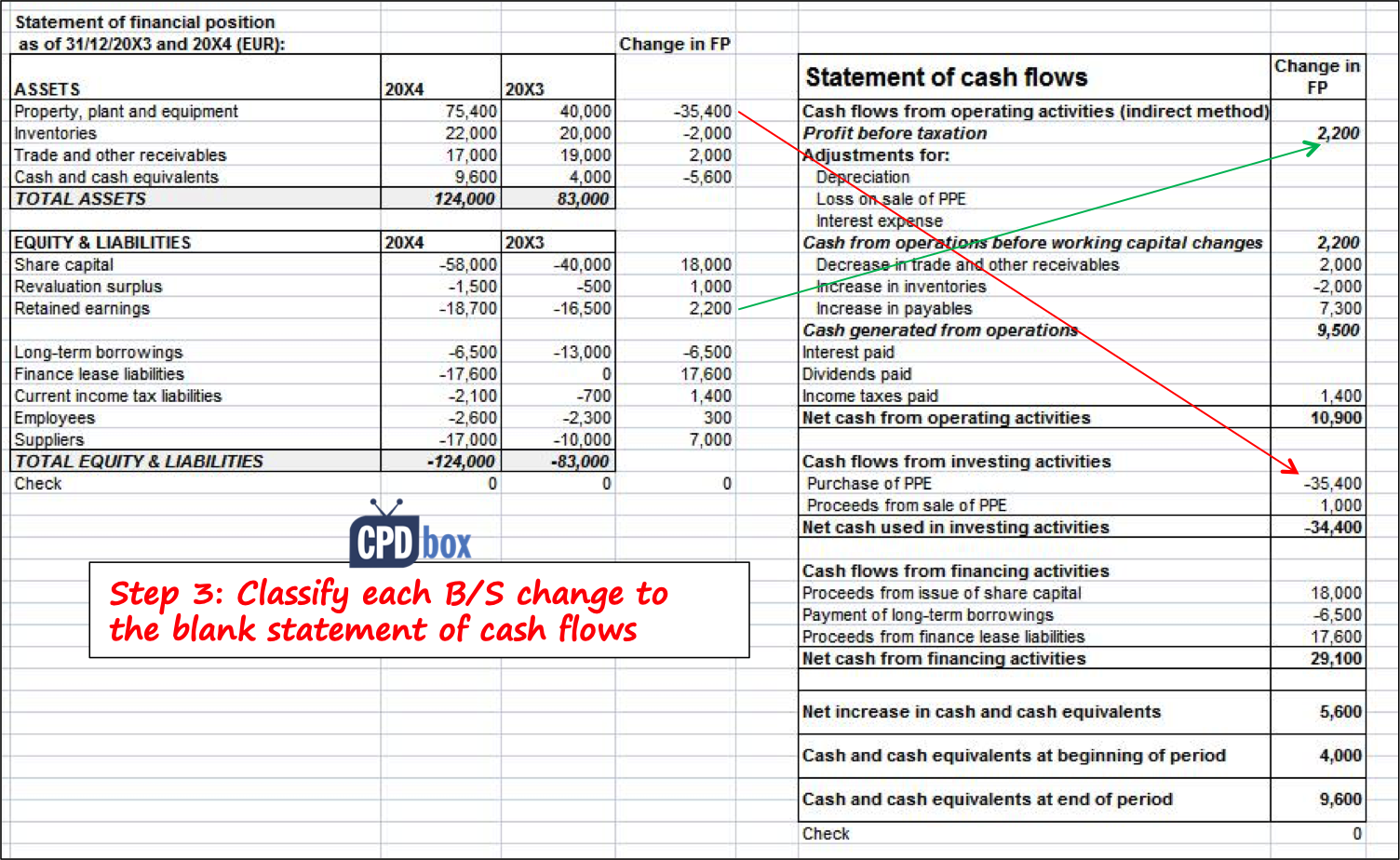

Overview of ias 7. Statement of cash flows. A vertical presentation of the numbers lends itself to noting the source of the numbers.

Classification of cash payments for deferred and contingent consideration arising from a business combination within the scope of. Learn the key accounting principles to be applied when preparing a statement of cash flows. The standard requires a complete set of financial statements to comprise a statement of financial position, a statement of profit or loss and other comprehensive income, a statement of changes in equity and a statement of cash flows.

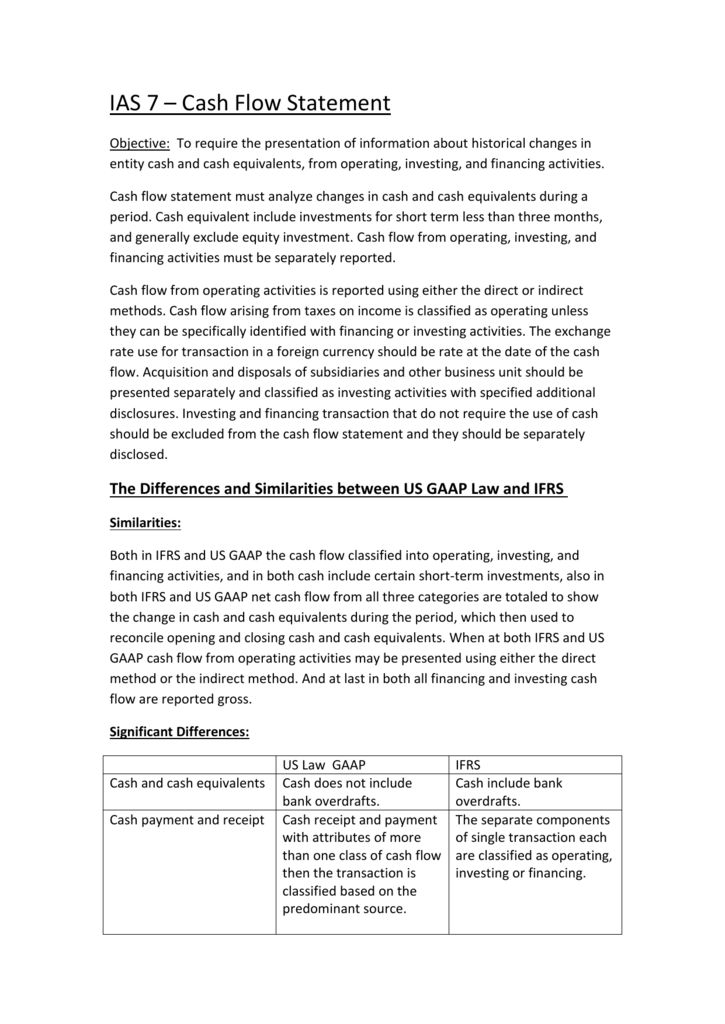

Flows’ (ias 7, the standard). Statement of cash flows in april 2001 the international accounting standards board adopted ias 7 cash flow statements, which had originally been issued by the international accounting standards committee in december 1992. Classification in the cash flow statements cash flows are classified under the three standard headings of operating, investing and financing activities.

Cash flows are usually calculated as a missing figure. Investing and financing transactions that do not require the use of cash or cash equivalents are excluded from a statement of cash flows but separately disclosed. It defines cash and cash equivalents and explains what is and what is not included in cash flow.

I would like to know how to treat finance costs when preparing my statement of. Statement of changes in equity. Cash, as defined in ias 7.6, comprises both cash on hand and demand deposits.

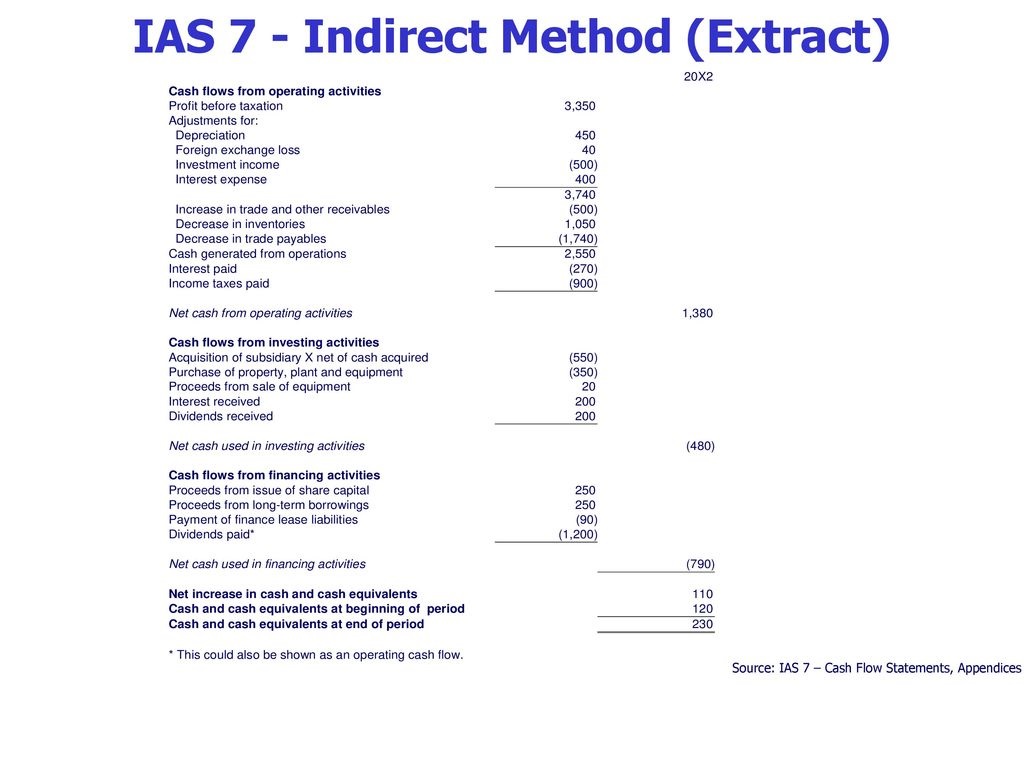

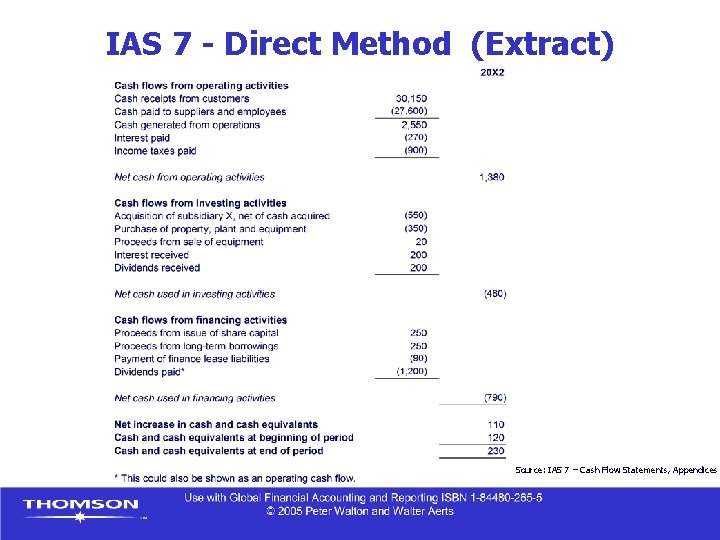

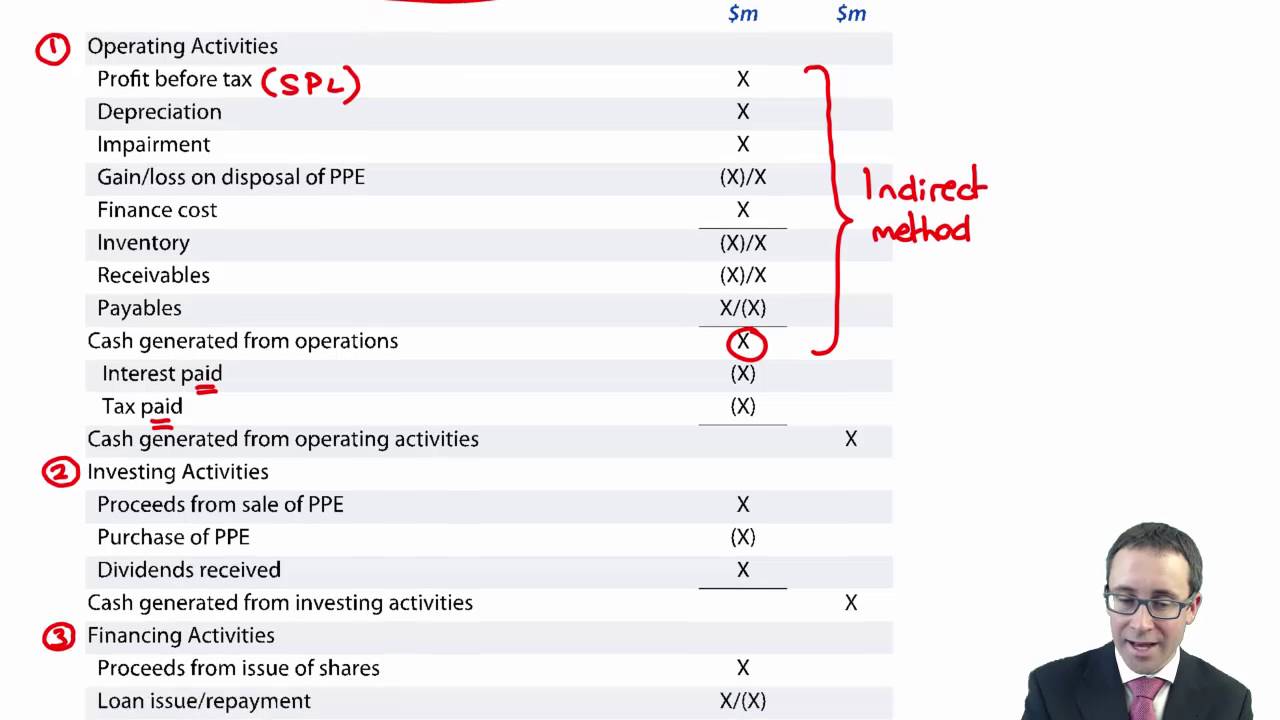

The definitions of these headings as per ias 7 are given below: Generate cash pay its creditors when they fall due pay dividends obtain finance, if required basic structure of a statement of cash flows a statement of cash flows shows the change in the amount of cash and cash equivalents held by the entity during the reporting period. The statement of cash flows shall report cash flows from (used in) financing activities ias 7.50 d an entity presents its entities are encouraged to report using the direct method.

Ias 7 Statement Of Cash Flows Objective Statements

Chapter 10 Cash Flow Statements Contents Q

Ias7 Cash Flow Statement Balance Sheet

Ias 1 Financial Statements Format Expense Cash Flow Statement

Cash Flows Statement Ias 7 Introduction And Operating Activities

Cima F1 Ias 7 Statement Of Cash Flows And Equivalents Youtube

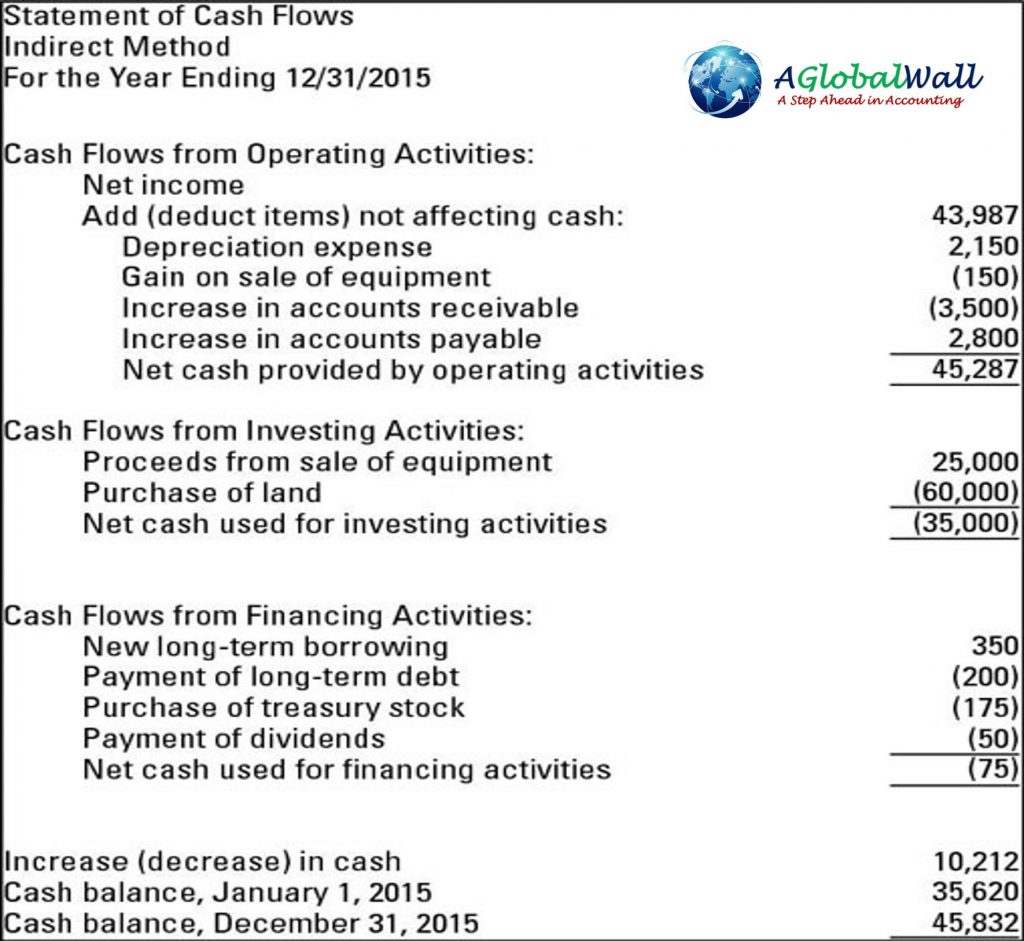

Ias 1 Presentation Of Financial Statements A Global Wall

Solution International Accounting Standard Ias 7 Statement Of Cahs

Ias 7 Statement Of Cash Flow

Ias 7 Para 18, Direct Method Cash Flow Statement, Reconciliation To

Ias 7 Cash Flow Statement Investing

Ias 7, Statement Of Cash Flows A Closer Look (pdf Download Available)

Ias 7 Para 18, Direct Method Cash Flow Statement, Reconciliation To