Fine Beautiful Info About Ias 1 Summary

Ias 19 Employee Benefits Summary Youtube

Ias 1 Presentation Of Financial Statements Summary 2020

Polity For Ias Session 1 Elementary Knowledge Mindmaps Iasmindmaps

Ias 1 Summary International Financial Reporting Standards

Ias 1 Presentation Of Financial Statements Acca Study Material

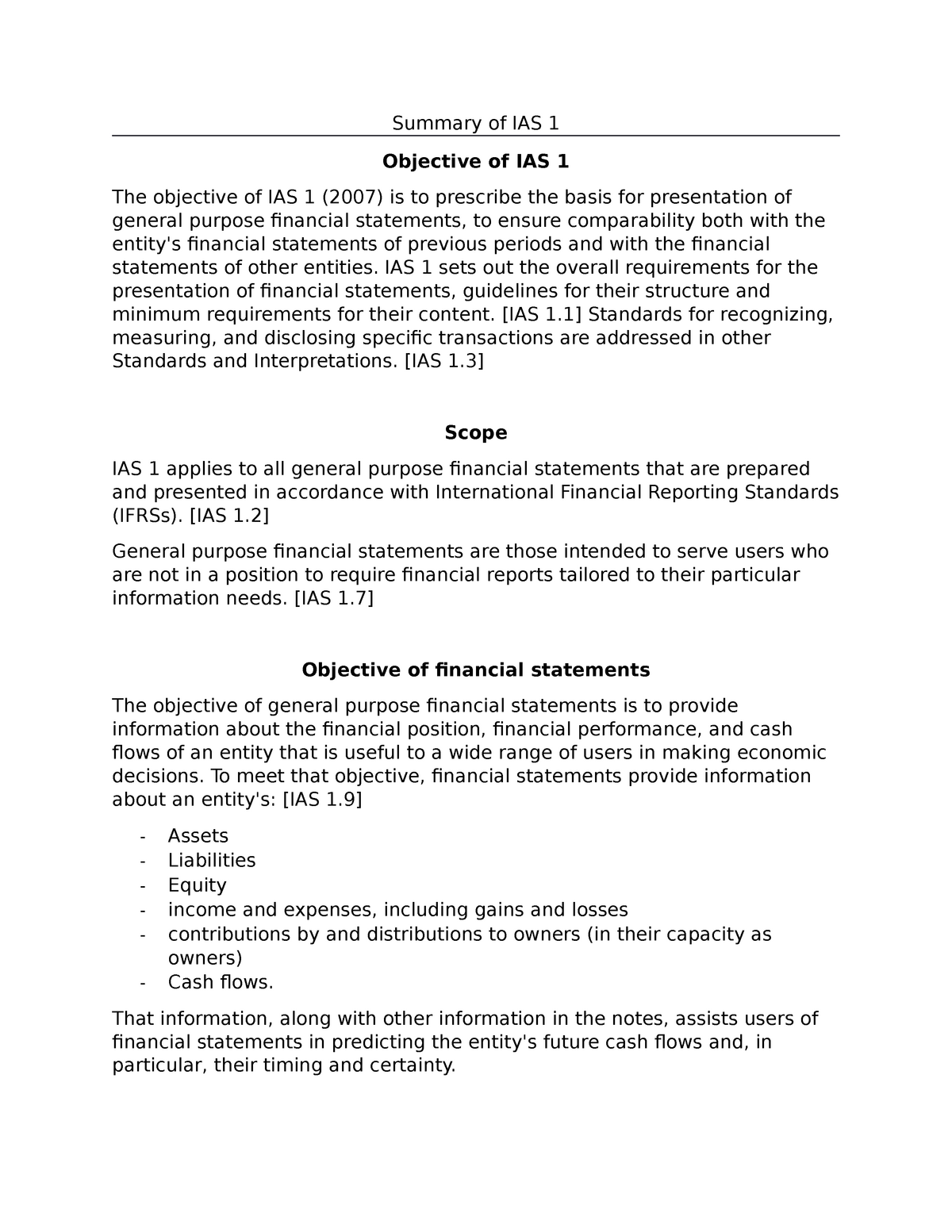

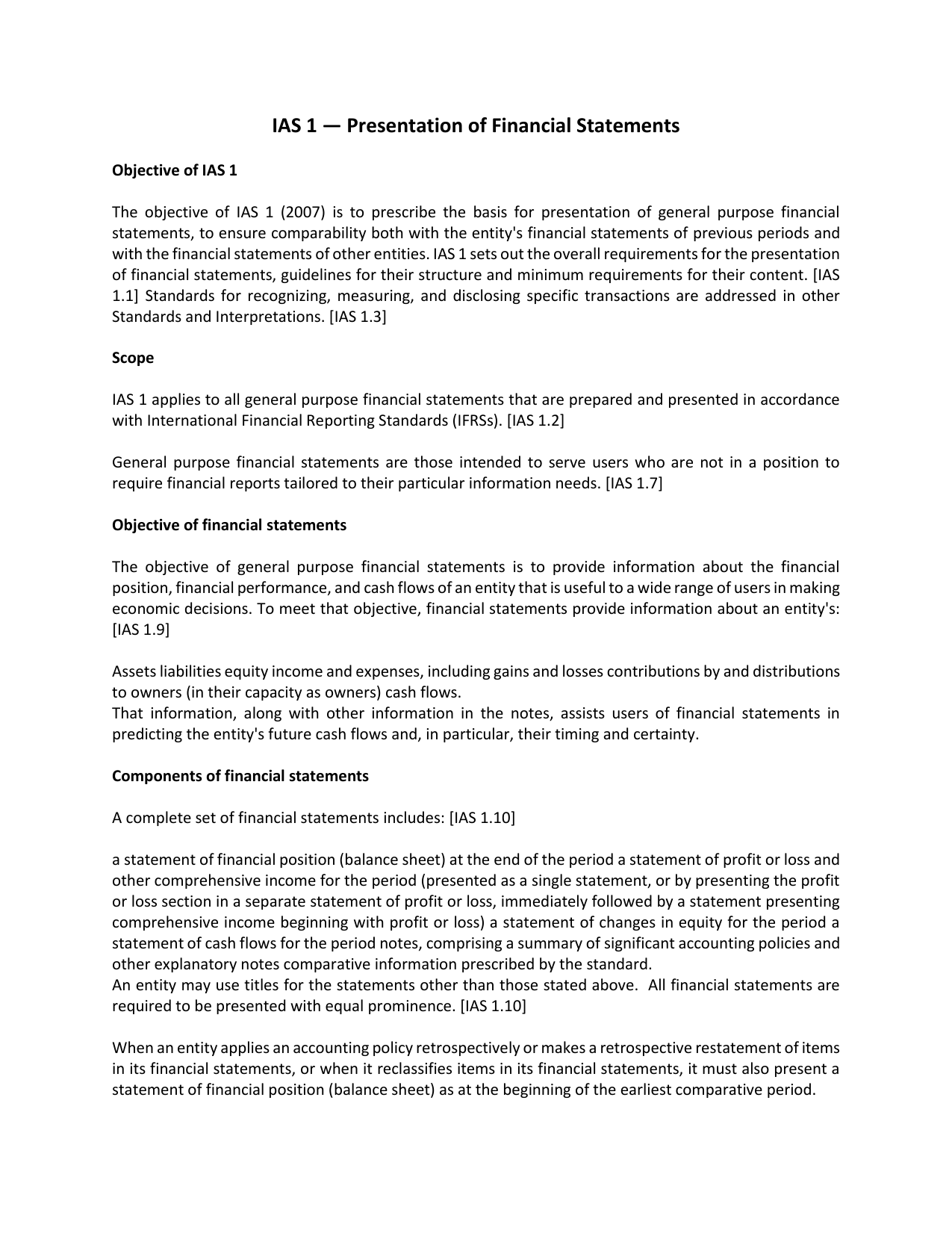

Ias 1 sets out overall requirements for the presentation of financial statements, guidelines for their structure and minimum requirements for their content.

Ias 1 summary. Seeking feedback on proposed topics for the ifrs accounting taxonomy update 2024. The statement of profit or loss and other comprehensive income, as the name suggests, presents profit and loss for the period as well as other. Superseded by ifrs 11 and ifrs 12 effective 1 january 2013.

It describes the general features of financial statements: It requires an entity to present a complete set of financial statements at least annually, with comparative amounts for the preceding year (including comparative amounts in the notes). International accounting standard 1 presentation of financial statements.

Ias 1 presentation of financial statements specifies how an entity is required to present its liabilities in the statement of financial position. International accounting standard 1 or also known as ias 1 it is an international financial reporting standard adopted by the iasb. It is applicable to ‘general purpose financial statements’, which are designed to meet the informational needs of users who cannot demand customised reports from an entity.

This standard prescribes the basis for presentation of general purpose financial statements to ensure comparability both with the entity’s financial statements of previous periods and with the financial statements of other entities. Ias 1 serves as the main standard that outlines the general requirements for presenting financial statements. Under existing ias 1 requirements, companies classify a liability as current when they do not have an unconditional right to defer settlement for at least 12 months after the reporting date.

Ias 1 primarily addresses the presentation of financial statements and can be divided into three large areas which include general guidelines going beyond presentation issues and general principles relating to presentation. In about you will find a brief summary and the history of the standard, alongside related active and completed projects and other related information. Summary of ifrs 1 objective.

The international accounting standards board (iasb) has removed the requirement for a right to be unconditional and instead now requires that a right to. Ias 1 sets out overall requirements for the presentation of financial statements, guidelines for their structure and minimum requirements for their content. Superseded by ifrs 7 effective 1 january 2007.

Ias 1 explains the general features of financial statements, such as fair presentation and compliance with ifrs, going concern, accrual basis of accounting, materiality and aggregation, offsetting, frequency of reporting, comparative information. Ias 1 presentation of financial statements (as revised in 2007) amended the terminology used throughout ifrs standards, including ifrs 1. Statement of cash flows;

Ias 1 presentation of financial statements. Feedback on ifrs accounting taxonomy 2023 proposed update 2. It requires an entity to present a complete set of financial statements at least annually, with comparative amounts for the preceding year (including comparative amounts in the notes).

The amendments to the practice statement also introduce this diagrammatic summary of the requirements of ias 1 concerning the disclosure of material accounting policy information: Ias 1 revised also requires a statement of financial position at the start of the earliest comparative period where there has been a retrospective adjustment to the accounts or reclassification of items. This standard prescribes the basis for presentation of general purpose financial statements to ensure comparability both with the entity’s financial statements of previous periods and.

Fair presentation and compliance with ifrs; The itcg discussed the following topics: Ias 1 presentation of financial statements:

Ias 39 Financial Instruments Recognition And Measurement Youtube

Ias 1 Provides Guidelines On The Presentation Of Pdf

Ias 10 Summary Events After The Reporting Period Financial

![[PDF] Comparison of IAS 39 and IFRS 9 The Analysis of Replacement](https://d3i71xaburhd42.cloudfront.net/67b3ca92d6a9916b419602abe09bd860d20fc48b/3-Table1-1.png)

[pdf] Comparison Of Ias 39 And Ifrs 9 The Analysis Replacement

Ias 2 Summary Inventory International Financial Reporting Standards

The Ultimate Guide To Finalizing Ias Ib ++tutors

Ias 1 Presentation Of Financial Statements Roundscript Consult

Ias 1 Summary Pdf

Ias 8 Accounting Policies, Changes In Estimates And Errors

Ias 17 Summary

Summary Of Ias 1 Final Project From Our Course (acc 1101)

Summary Of Ias 1 International Financial Reporting Standards

Ias 1 Summary